Remember how exciting it was to buy your first place? It felt like crossing a long-awaited finish line. It gave you a place to build your life. Maybe it’s where you lived when you got married. Or where you welcomed a child or a pet into the family.

But that was just the beginning.

For most people, your first house was never meant to be your forever home. It’s a stepping stone for what comes next.

And if your life looks different today than it did when you got the keys, you’re not stuck. Moving may be more realistic than you think.

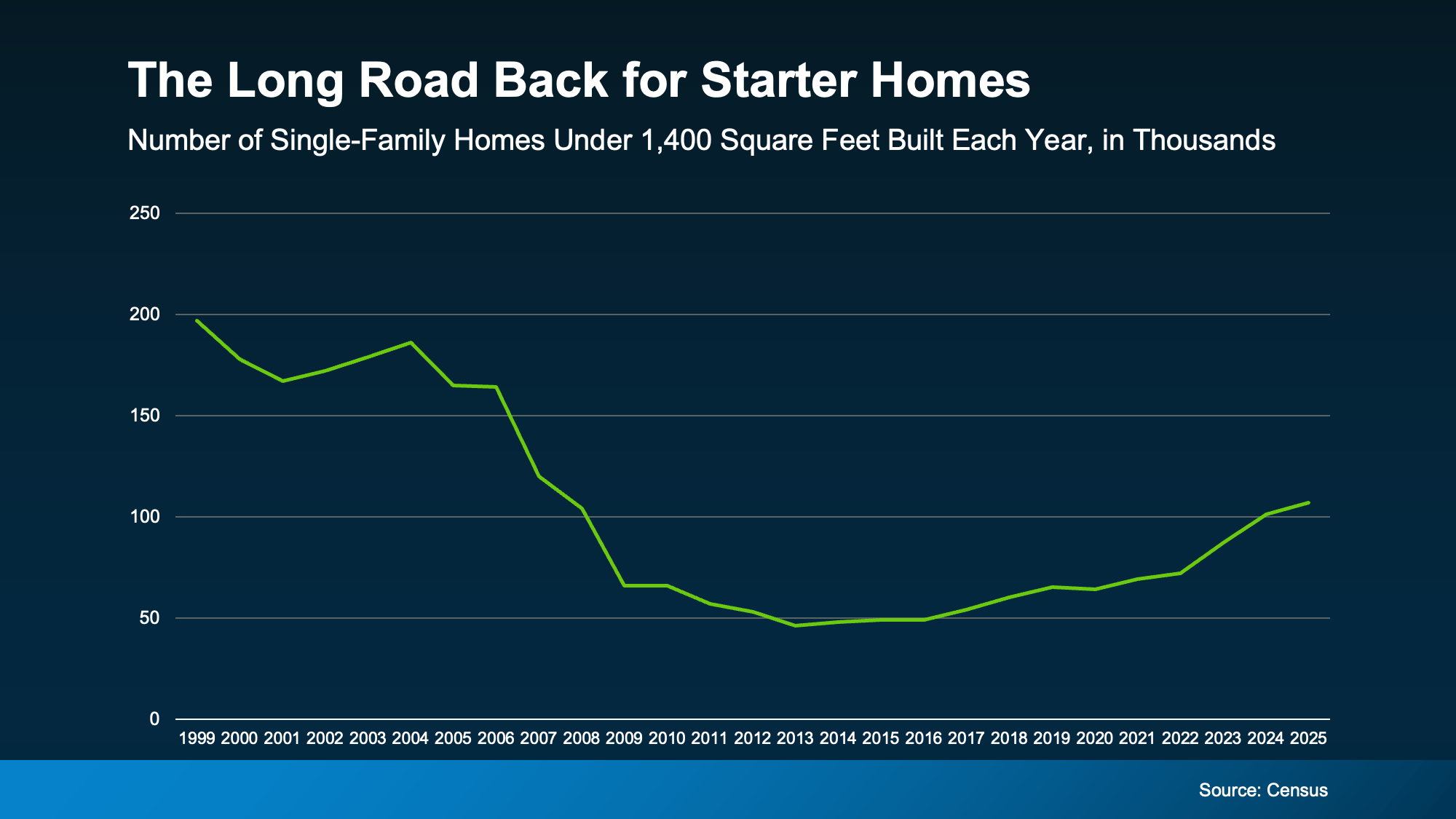

Starter Home Inventory Is Still Relatively Low

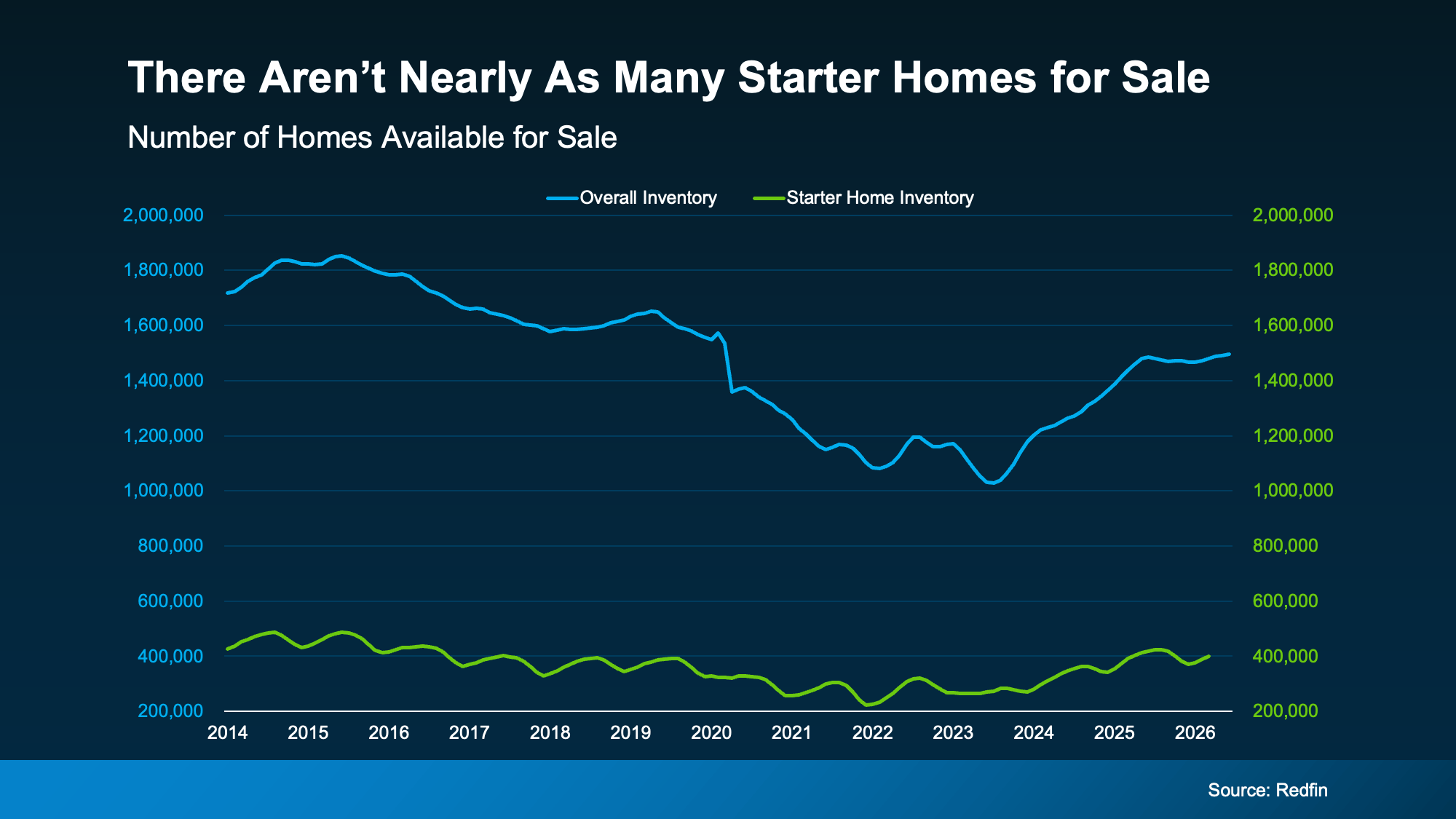

If you’ve been wondering whether now is the right time to move up, here’s something worth knowing. Starter homes remain one of the hardest types of homes to find. And that’s good news if you’re thinking about selling your first place.

Historically, we haven’t been building enough homes for first-time buyers. And even though homebuilders have shifted more attention toward smaller, entry-level homes lately, the Census shows there’s a long way to go to re-build supply (see graph below):

That means your current house is in demand – and that’s a dream scenario for sellers. But that’s only half the story. You also need somewhere to go.

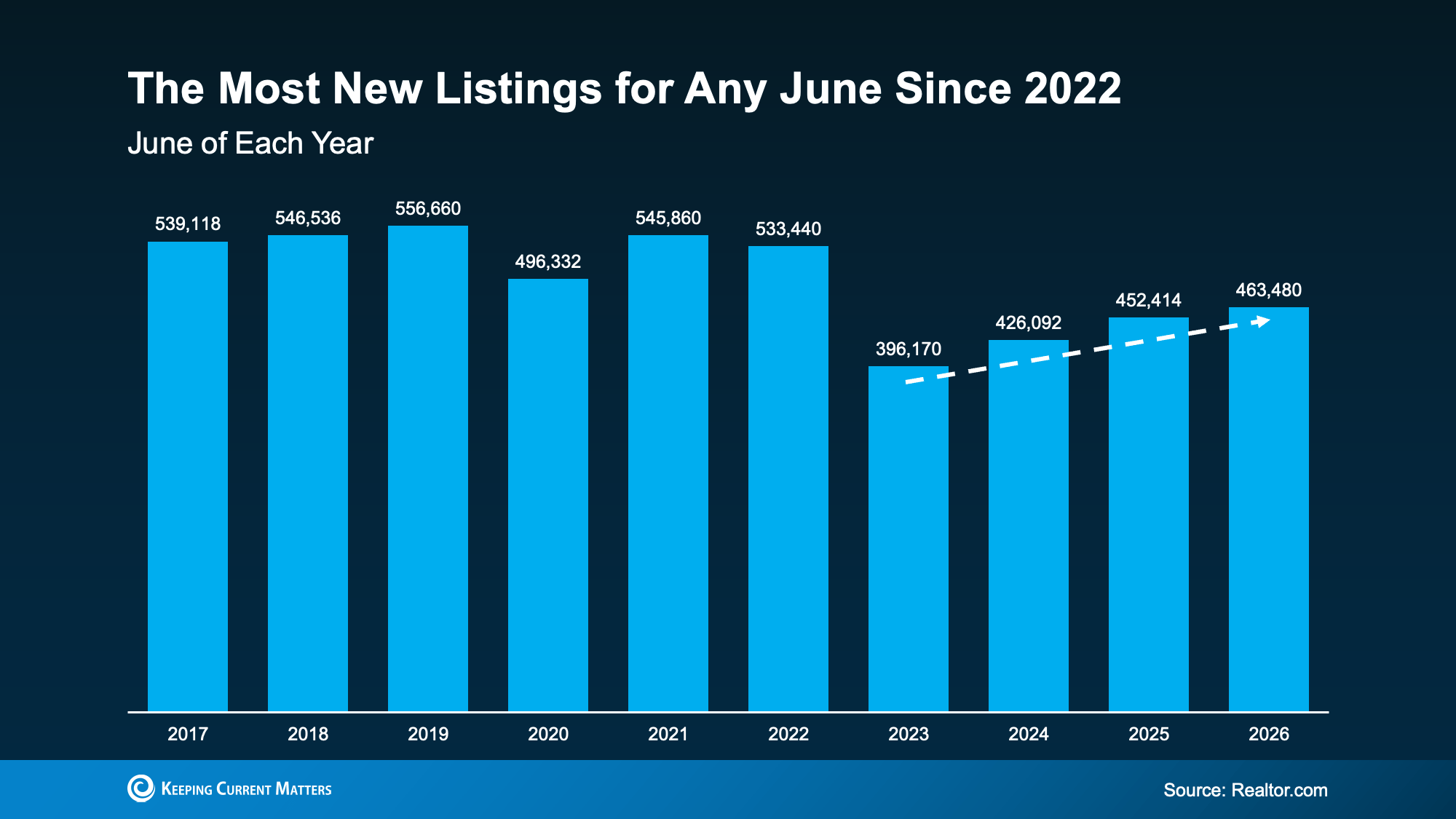

There Are More Move-Up Homes on the Market

Here’s where this gets interesting. While the supply of starter homes remains tight (the green line), data from Redfin shows that the number of homes for sale has been climbing overall (the blue line):

As Nadia Evangelou, Principal Economist and Director of Real Estate Research at the National Association of Realtors (NAR), explains:

“Too much of the inventory available today remains concentrated at higher price points, leaving a shortage of options for entry-level and middle-income buyers.”

That means you may have more choices for your move up than you’d expect. Whether you’re hoping for another bedroom, a home office, a bigger backyard, or simply more room for this next stage of life, today’s market may finally be giving you the chance to find it.

At the same time, your current house may be exactly what someone else has been looking for because homes like yours are still in short supply. That’s a unique advantage for move-up buyers. And it could help you sell for a stronger price. As Zillow says:

“Starter home value appreciation has outpaced other types of homes nationally, mostly because they’re so in demand.”

Your Biggest Advantage May Be Your Equity

Here’s the cherry on top. There’s one more thing your first home has been doing behind the scenes, and that’s building equity. Every mortgage payment you’ve made and every year your home’s value has grown has quietly increased your ownership stake in your house.

According to Cotality, the average homeowner with a mortgage has $295k in equity built up. While your number may be different, once you sell, it could become the down payment on your next home or help reduce the amount you need to borrow at today’s rates.

Put it all together and your move up becomes a lot more realistic than you think:

-

The house you’re selling is in demand.

-

The house you’re buying may be easier to find.

-

And the equity you’ve built can help bridge the gap between the two.

Your first home did exactly what it was supposed to do. It gave you a place to start.

Now, it may be the thing that helps you take the next step.

Bottom Line

Your first home was never meant to be your forever home. It was meant to help you build a life and build the financial foundation for whatever came next.

If your current home no longer fits the life you’re living today, connect with an agent. You may be closer to your next chapter than you realize.