Buying or selling a home is a big financial decision. And right now, it feels even bigger. Inflation is high, costs are high, and you want to be sure the timing is right before you make your move.

But if you do decide to go for it, whether you’re buying or selling, here’s something reassuring to hold onto. Not only does your move change your own life, but it also gives your whole community a boost.

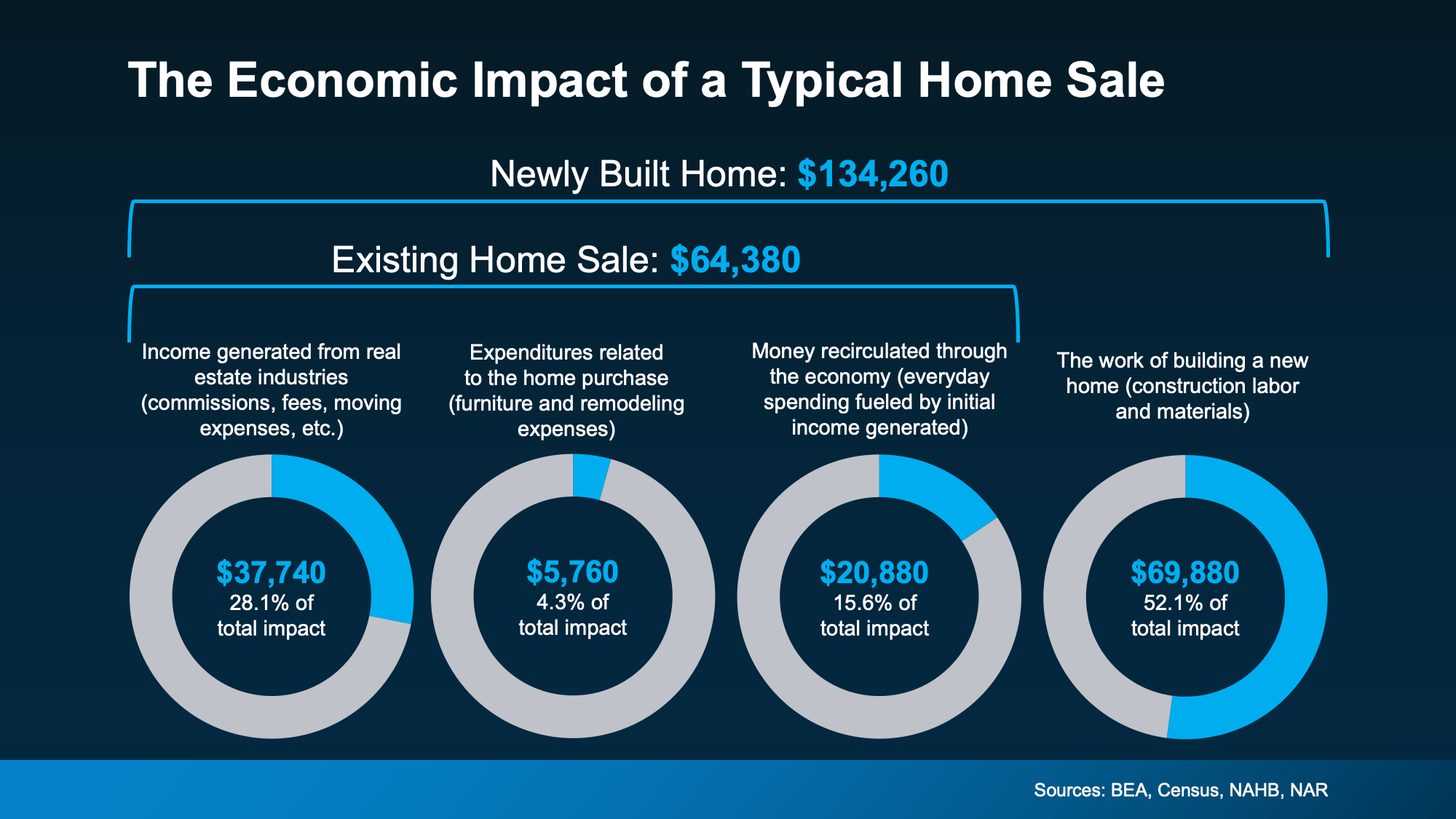

Real estate is a huge part of the economy. In 2025, it added up to about $5.6 trillion, according to the National Association of Realtors (NAR). A good share of that comes from everyday people buying and selling homes, just like you.

Your Move Puts Real Money Into the Local Economy

Every sale sends money flowing through your area. NAR data shows that buying an existing home (one that’s already been lived in) adds about $64,000 to the local economy. Buy a newly built home, and that number climbs to more than $134,000 (see graph below):

Over half of that comes from the work of building the home itself. The rest flows to real estate services, like agent and lender fees, plus what you spend settling in afterward, on things like furniture and remodeling.

And the money doesn’t stop there. As local businesses earn it, they spend it again in your area, so a single sale ripples further than the sale price alone.

One Sale Keeps a Lot of People Working

Behind every sale is a whole network of people doing their jobs. Contractors, lenders, inspectors, movers, and more. When you buy or sell, you help keep them busy. Lawrence Yun, Chief Economist at NAR, puts it this way:

“Increased home sales mean more economic activity — lawn care, furniture purchases, moving services, mortgage originations and other related business activities all get a boost.“

So, your move supports your neighbors’ livelihoods, too. The deal that gets you into your next home also helps a local crew make payroll. In a year when every paycheck counts, that’s no small thing.

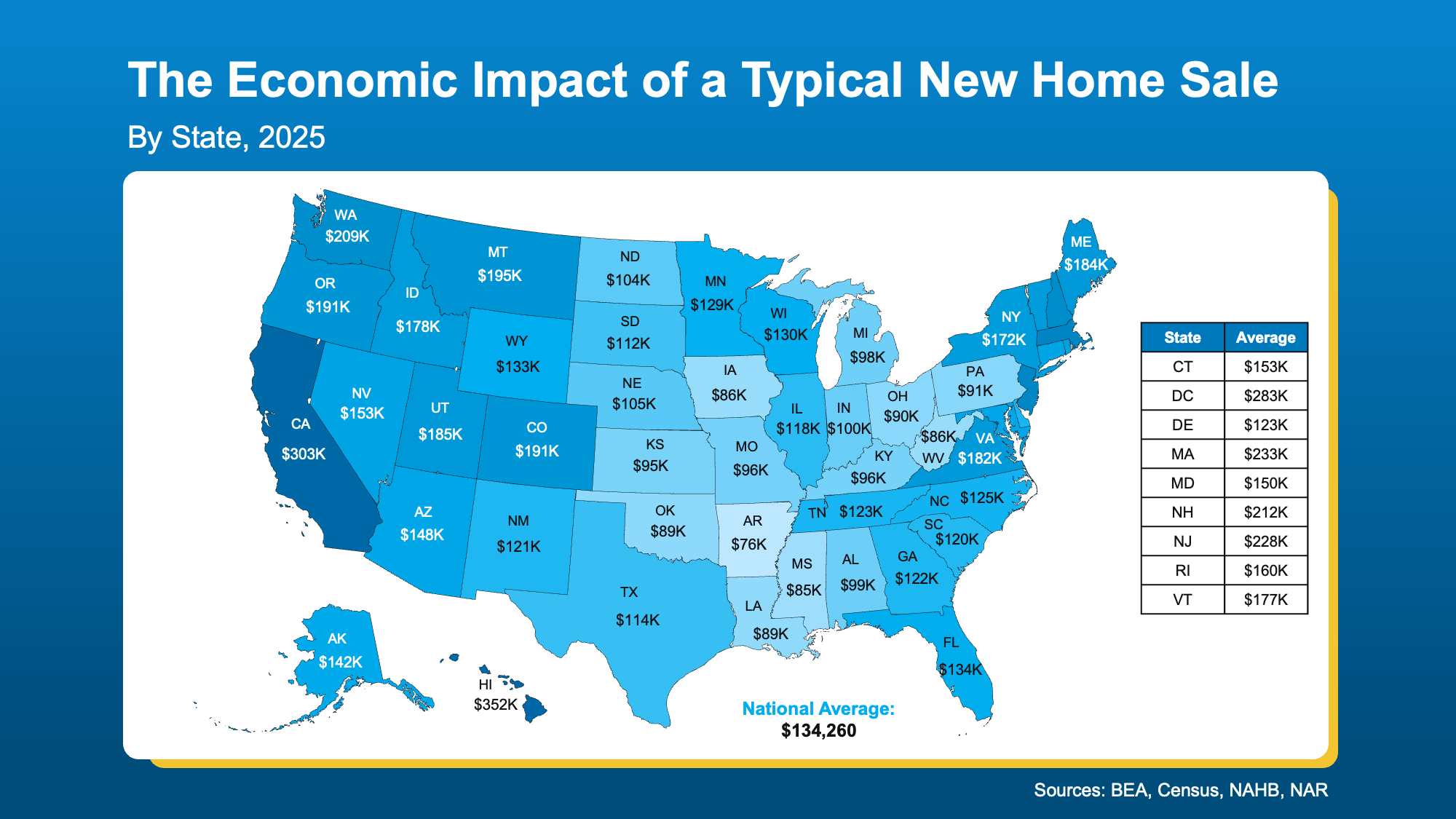

Your Local Impact May Be Even Bigger

What your move financially adds to your community depends a lot on where you live. To help you see how it can vary, here’s a look at the impact of a typical newly built home sale by state.

The national average for a newly built home is about $134,000, but some states see far more (see map below):

In California, a single sale adds more than $300,000 to the local economy. In Hawaii, it’s over $350,000. Even in the most affordable states, the number lands in the tens of thousands.

Want to know what a move would mean where you live? A local agent can show you the figure close to home.

Bottom Line

Moving is both a personal milestone and an investment in your community. So, if the time is right for you, connect with a local agent. You’ll make a difference for more people than you know.

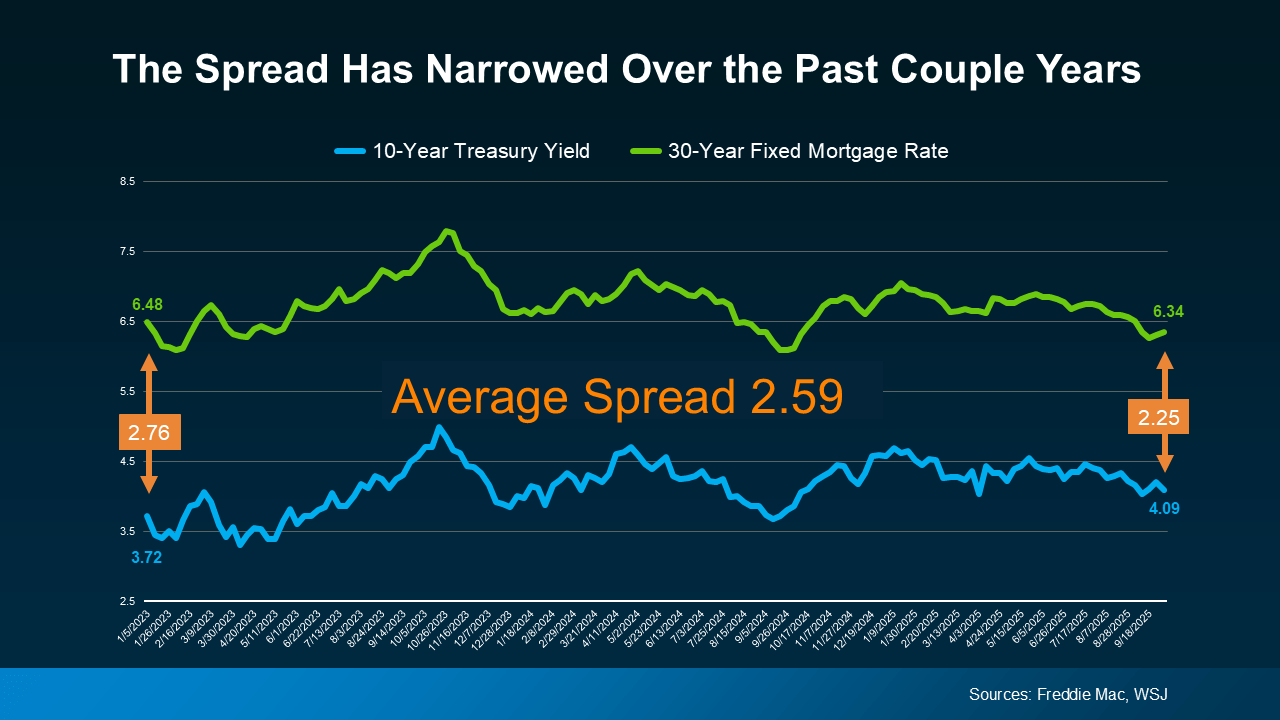

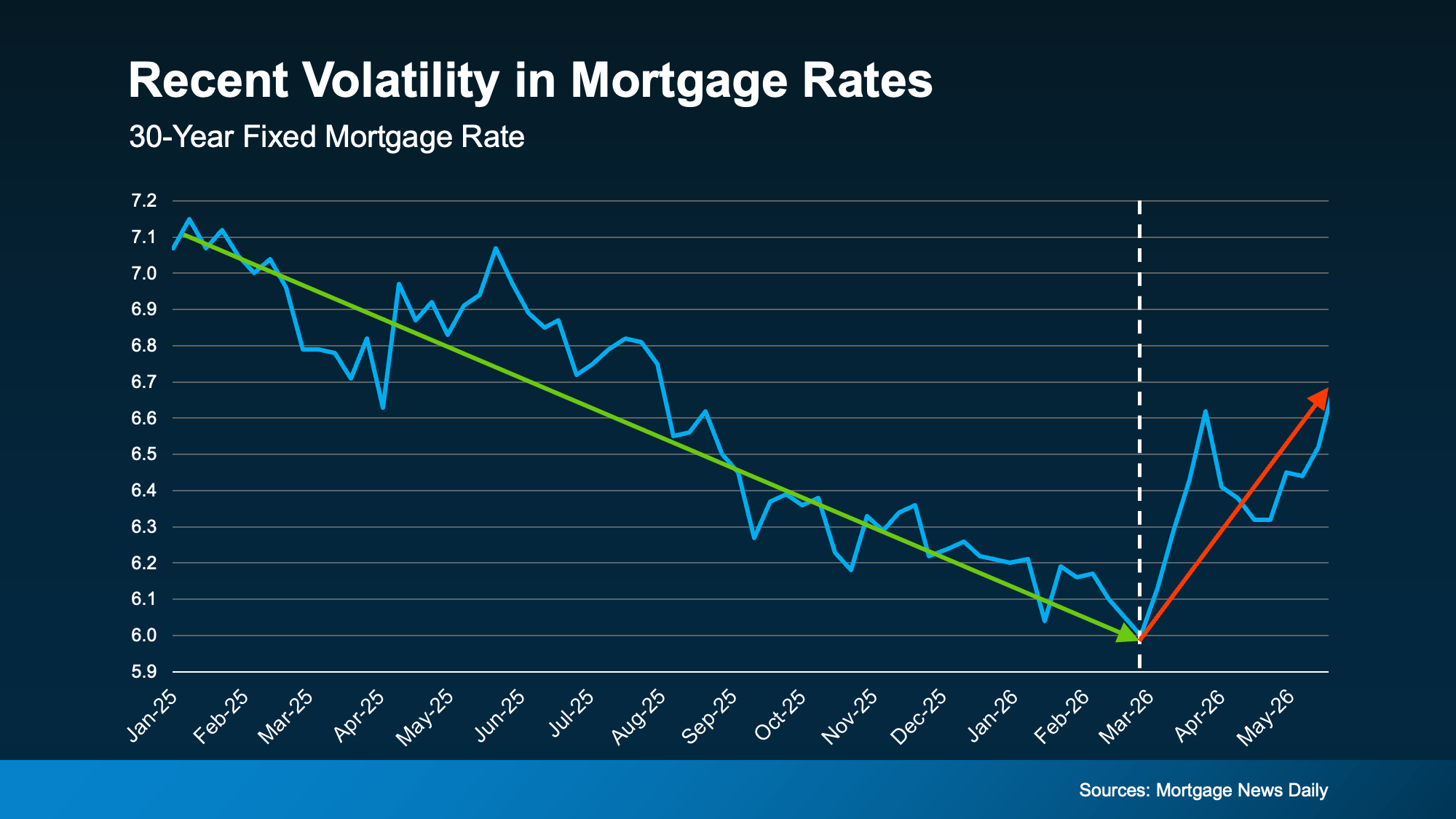

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?