Today’s home prices have a lot of buyers – especially first-time buyers – wondering if there’s even anything out there that’s in their budget. But owning a home may be more within reach than you think. Sometimes, it just means considering a different type of home.

Condos and townhomes can be a great way to buy without stretching every last dollar. And right now, two things make them worth a serious look.

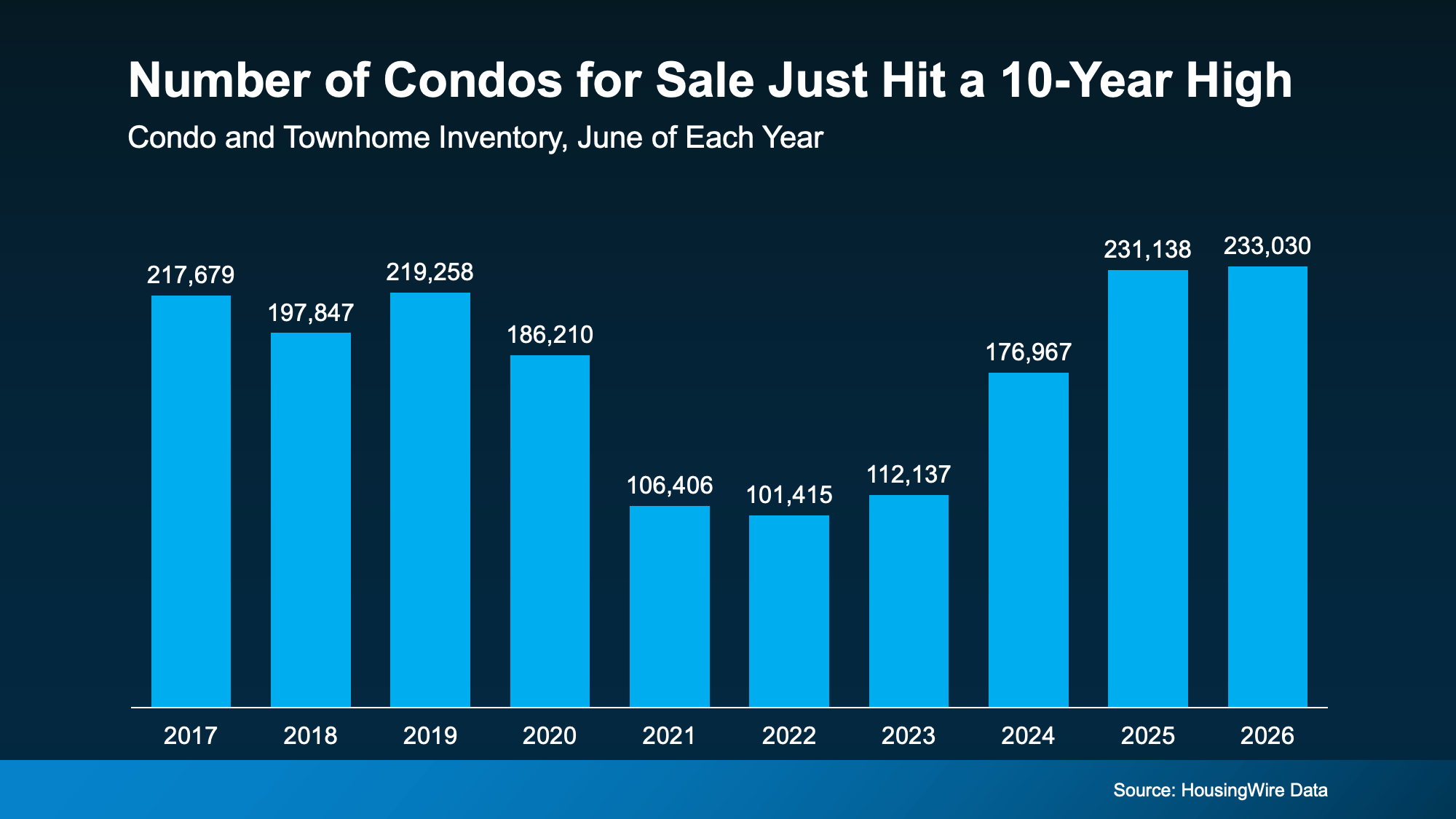

There Are More Condos and Townhomes To Choose From

Maybe you feel like there’s just nothing out there for you, and you’ve exhausted all your options. But have you considered condos or townhomes? A lot of buyers start by looking for a single-family, detached home without even realizing what that search omits from their pool of choices.

According to HousingWire Data, there were 233,030 condos and townhomes for sale this June. That’s more than any June in at least the past decade, and more than double the number available back in 2022 (see graph below):

That means there are more options out there in this segment of the market – and that’s especially good news for first-time buyers. These types of homes can be a great way to break into the market for less.

Just remember, that’s the national number. What’s available will depend on where you’re looking. But generally speaking, more options means less competition, more time to decide, and more room to negotiate.

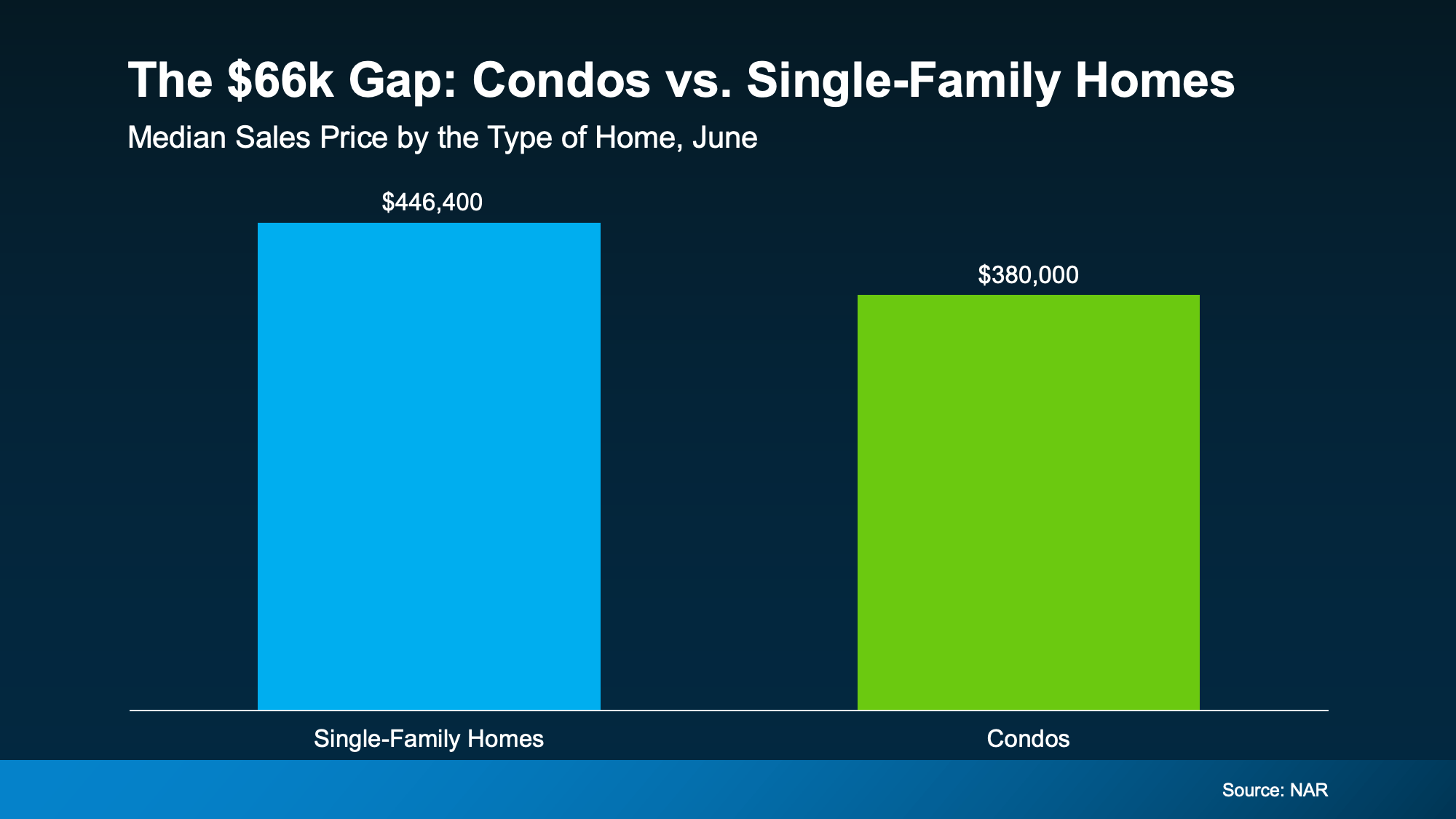

They Also Tend To Cost Less Than Single-Family Homes

Price is the other big draw. According to the National Association of Realtors (NAR), the median condo price was $380,000 in June. In contrast, the median single-family home price was $446,400 (see graph below):

That’s a difference of more than $66,000.

A big reason why? Condos are usually smaller than single-family homes. And smaller homes can come with smaller price tags.

And if you don’t need all that extra space, that lower entry price could be exactly what gets you through the door.

Condo or Townhome? How They’re Different.

For buyers who feel priced out of the market, a condo or townhome could be a way in. But there are some things to know. Before you start checking out homes, it’s good to understand how these two compare to each other – and to a single-family home.

-

With a single-family detached home, you own the house and the land it sits on, and you don’t share any walls with neighbors. That means the most space and privacy. But it also usually comes with a higher tag, and all the maintenance is on you.

-

With a townhome, you own the building and the lot it sits on. They’re usually multi-level, so you get more space, and you share two walls at most. You’ll also have more say over how your home looks and how repairs get done, but more of that upkeep falls on you.

-

With a condo, you own just the inside of your unit and may have access to community features like a pool or gym. The building and shared space belong to everyone who lives there, which means you have less maintenance responsibilities. But you’ll also likely have more neighbors around you, less control over building decisions, and higher HOA fees since the HOA handles the exterior and common areas.

Bottom Line

A condo or townhome could be your path to owning a home without blowing your budget. Connect with a local real estate agent to see what’s for sale in your area and figure out which type of home fits your lifestyle, and your bottom line.

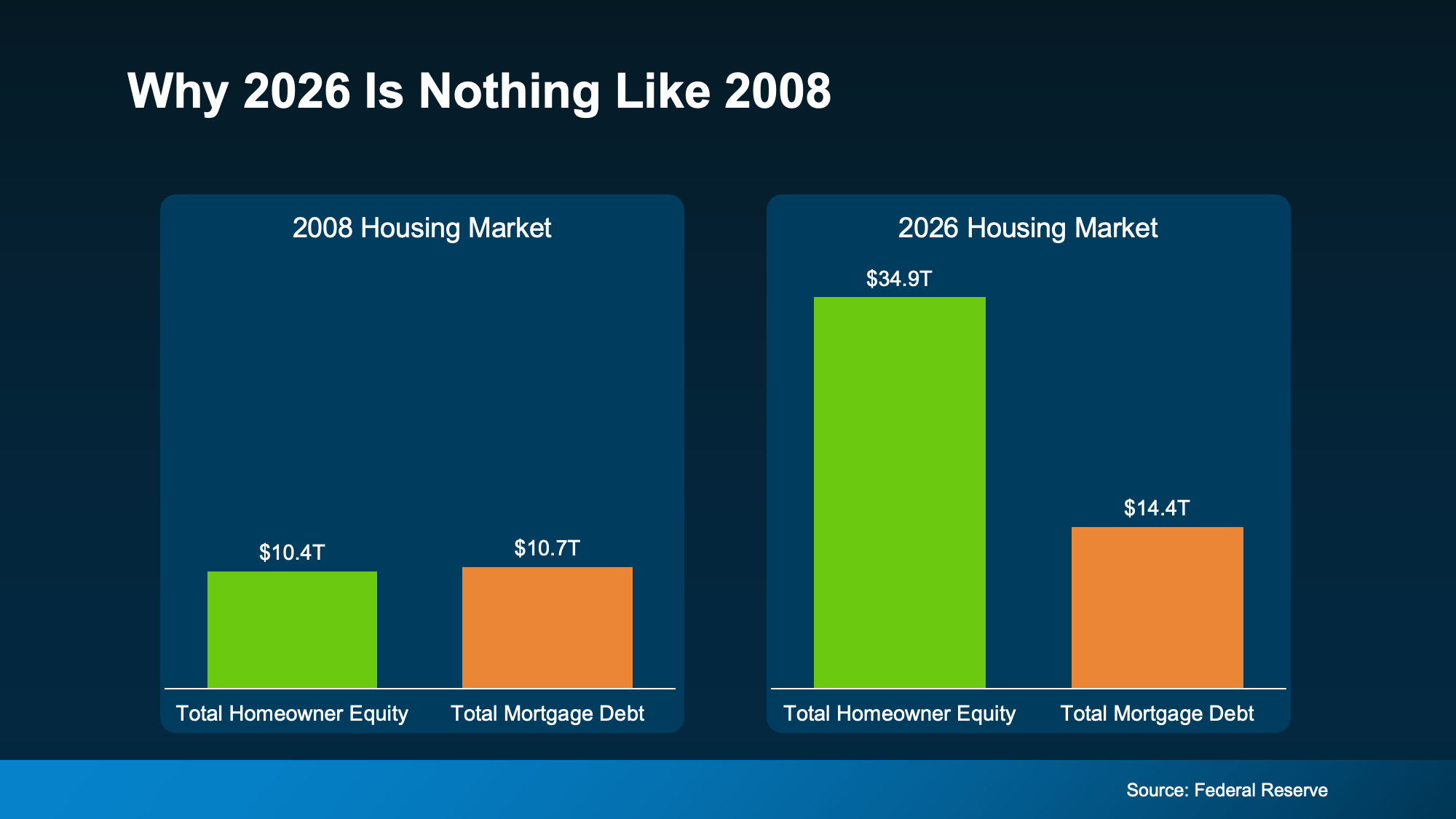

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time. That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

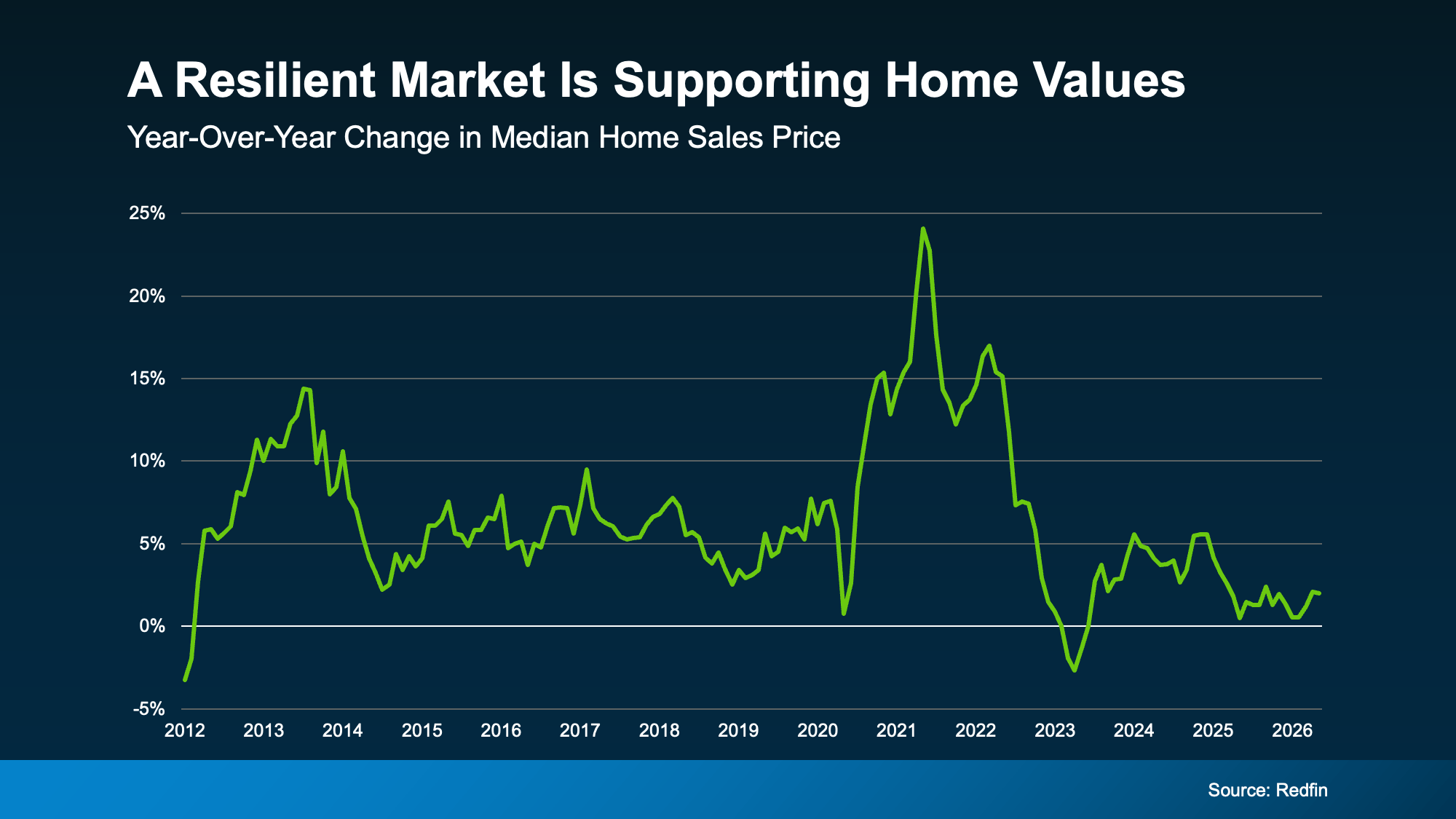

That’s a big reason inventory stays tight. Those homeowners aren’t in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling. That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

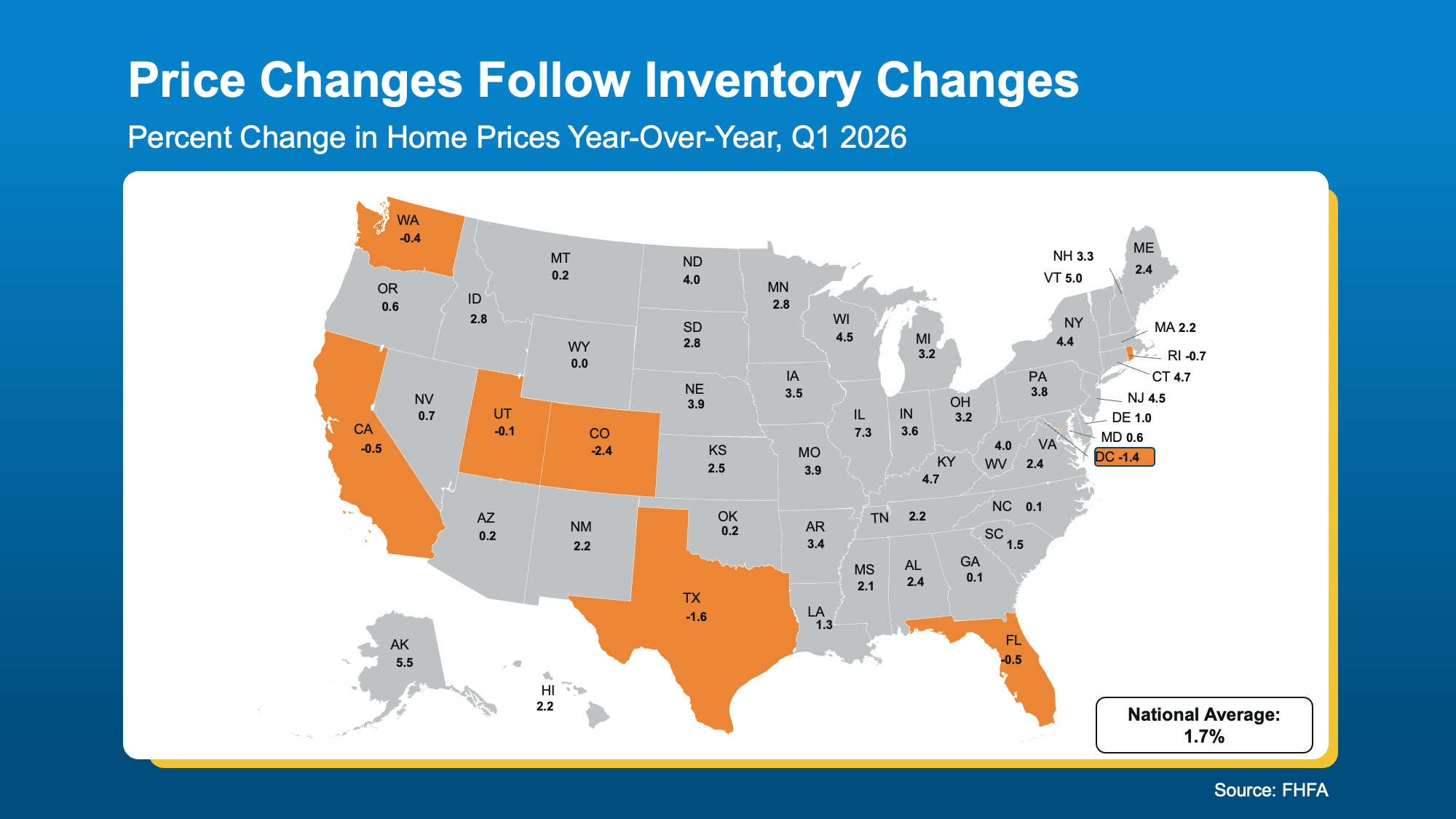

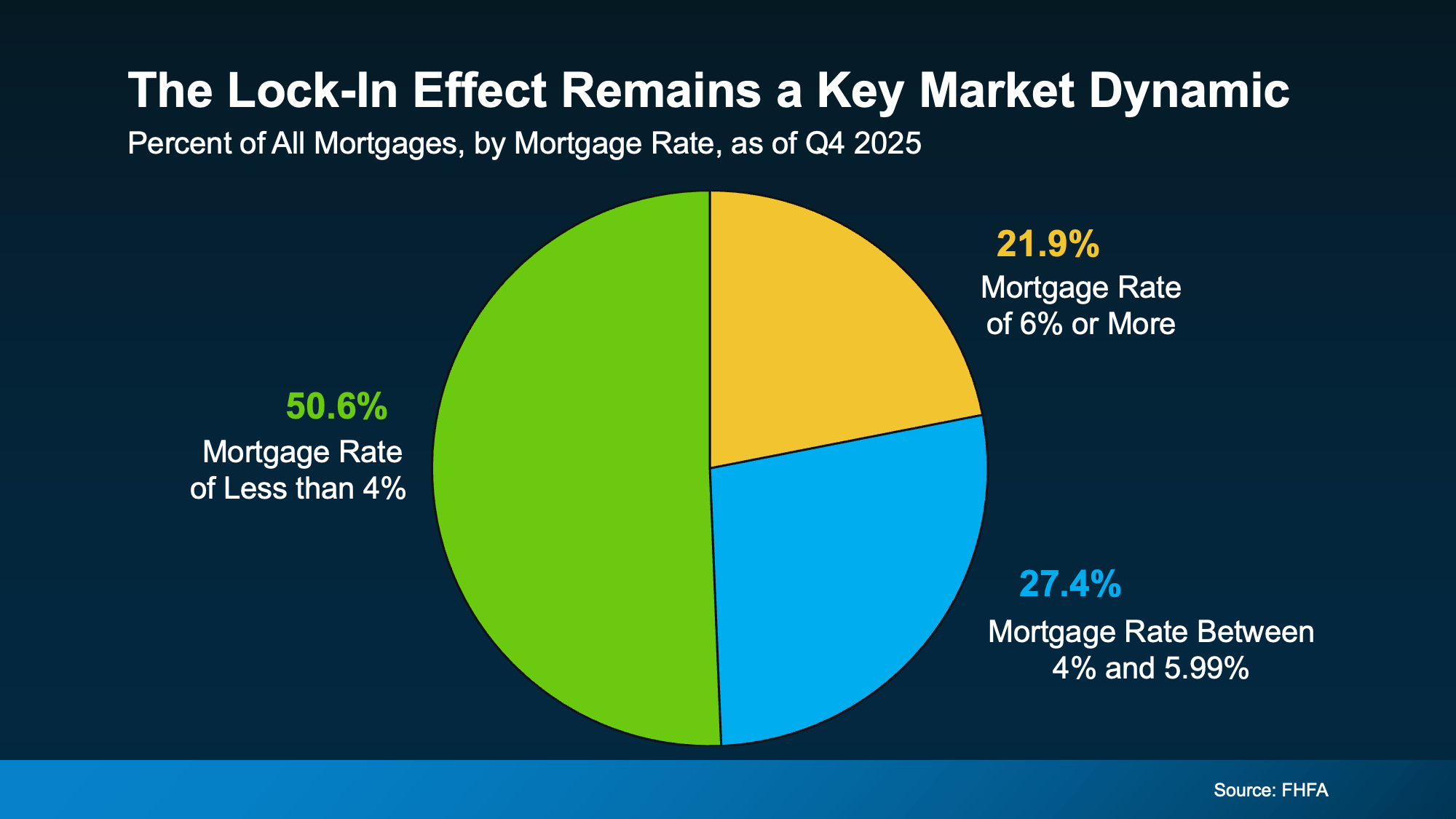

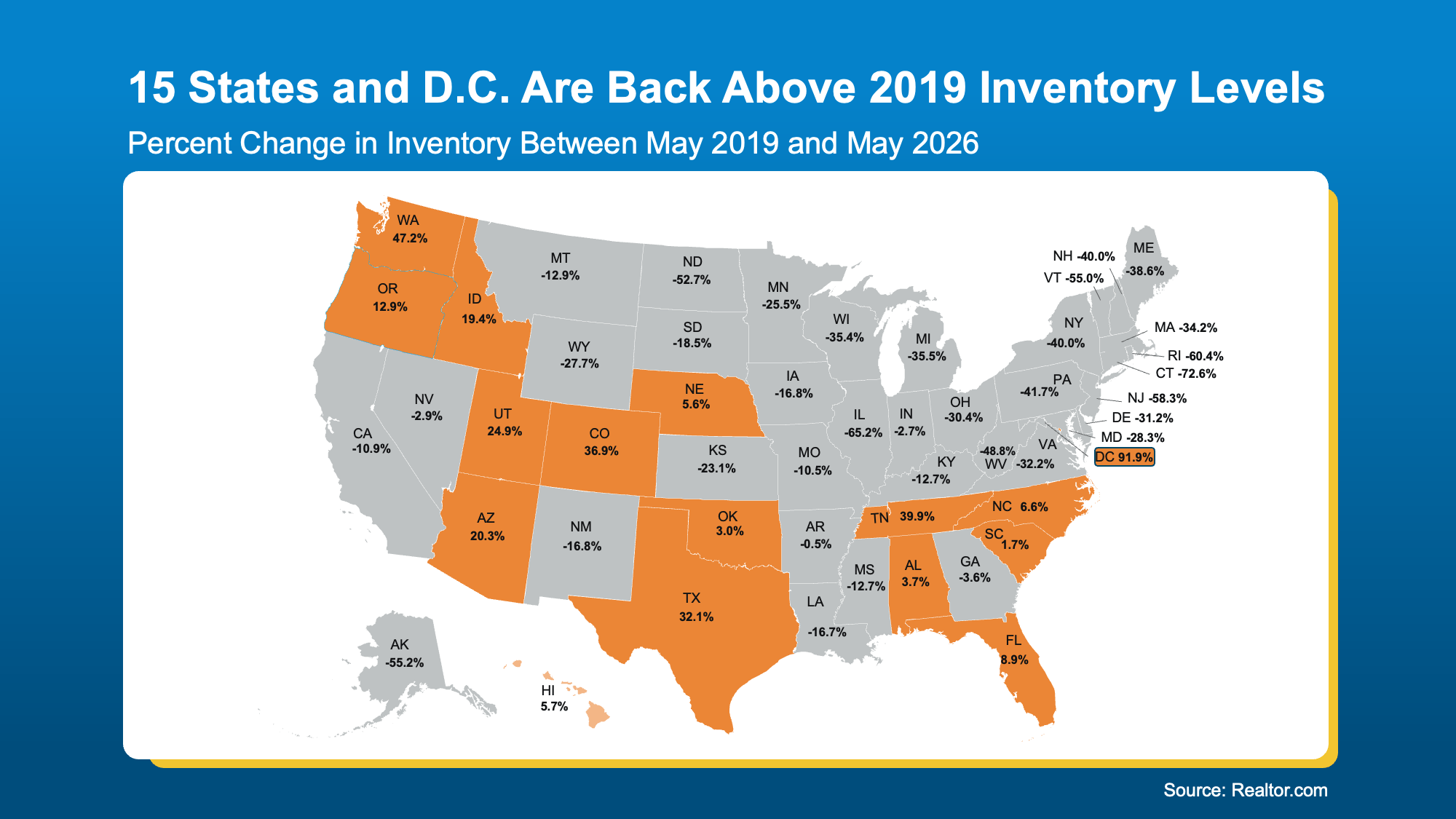

Now, let’s look at the latest Federal Housing Finance Agency (FHFA)

Now, let’s look at the latest Federal Housing Finance Agency (FHFA)