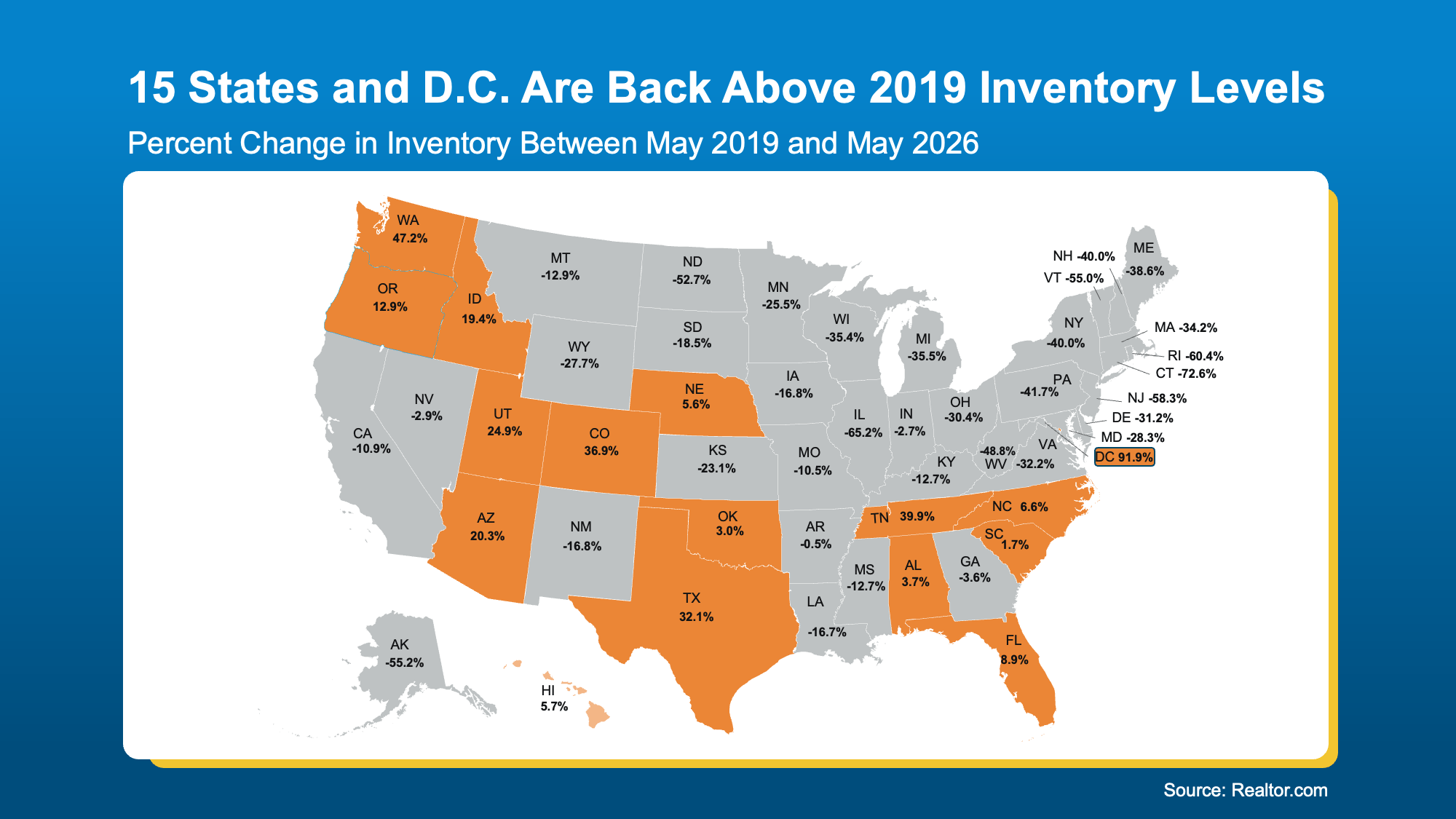

Negotiations are back. More buyers are asking for better deals, and more sellers are giving them. Builders are throwing in extras, too.

That’s why whether you’re buying or selling today, there are two terms you’ll hear a lot: concession and incentive.

-

A concession is something a seller agrees to during negotiations to get a deal done.

-

An incentive is a perk a builder (or a seller) advertises upfront to attract buyers.

Let’s run through what you need to know about both and how they could play a role in your move.

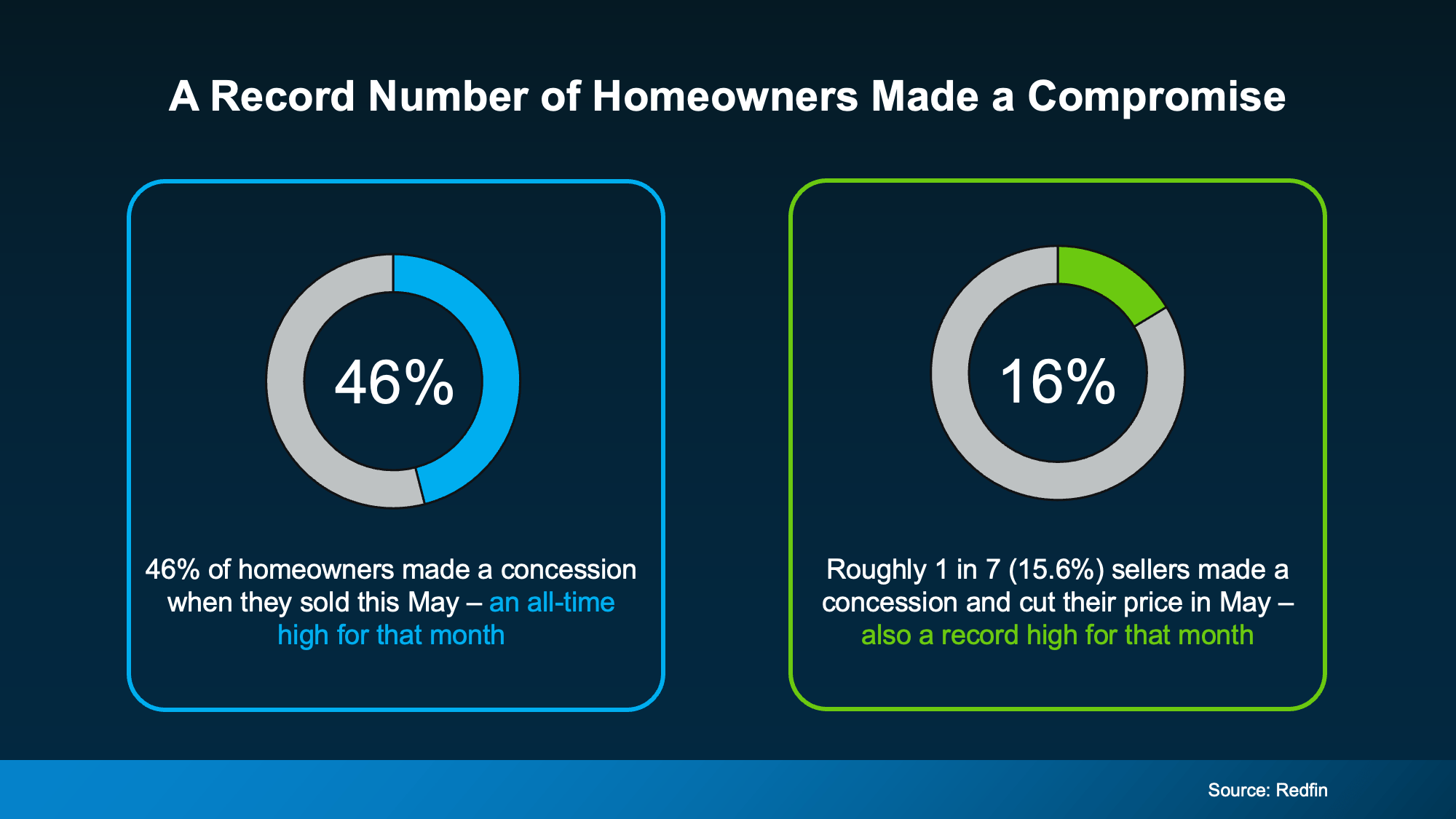

More Sellers Are Agreeing to Concessions

Almost half (46%) of homeowners who sold recently gave the buyer a concession, according to Redfin. That’s the highest share on record for this time of year. And roughly 1 in 7 (16%) sellers went a step further, cutting their asking price and offering a concession on top (see chart below):

So, what kind of concessions are we talking about?

A seller might cover part of your closing costs, take care of a repair, or offer a credit that trims your upfront costs. It’s how they keep a deal on track when buyers have more options to choose from – and homeowners aren’t the only ones compromising.

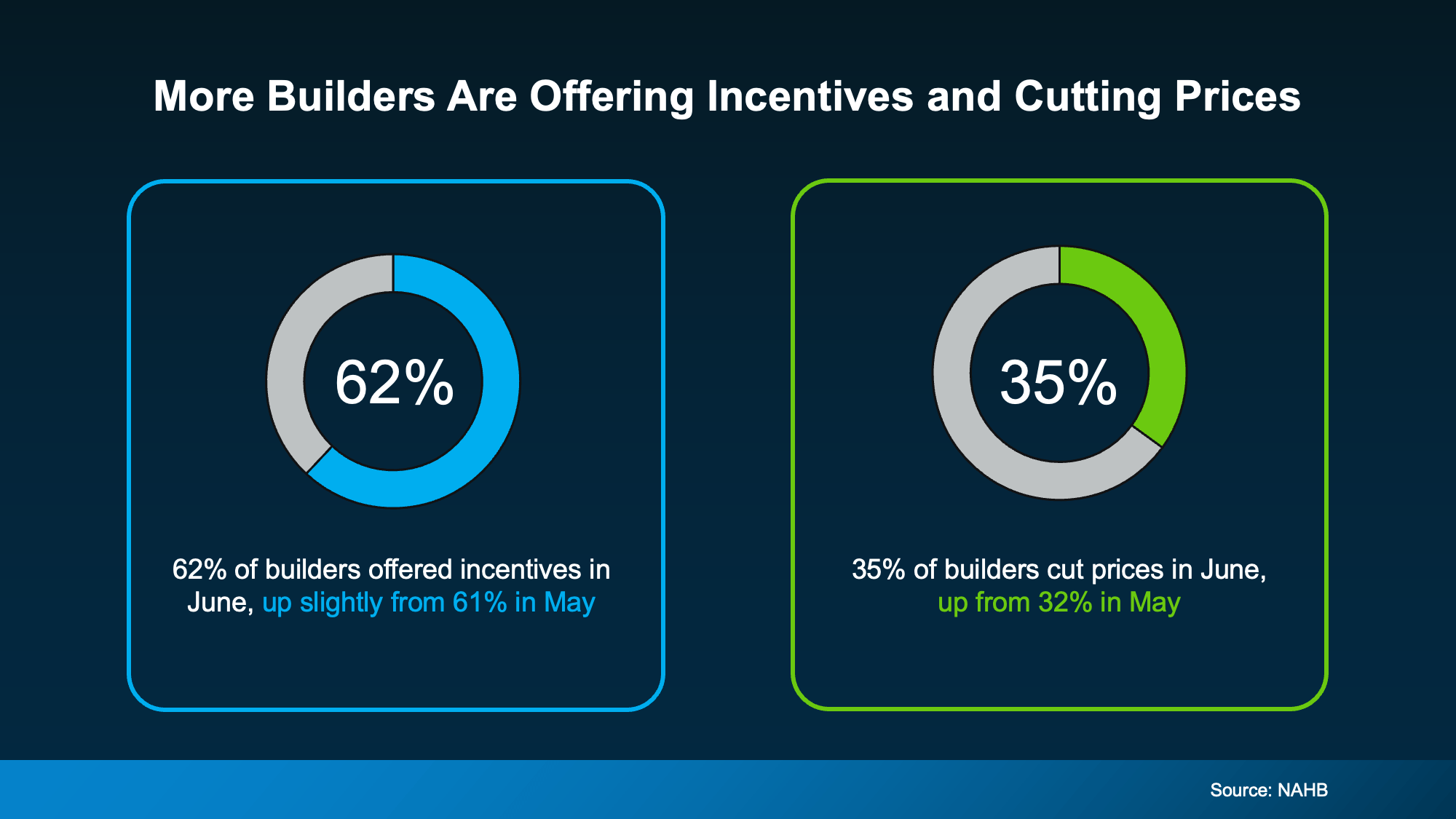

Builders Are Cutting Prices, Too

Newly built homes are seeing the same push and pull. According to the National Association of Home Builders (NAHB), 62% of builders are offering incentives right now. And about 35% are cutting prices outright (see chart below):

Those incentives often look like:

-

Mortgage rate buydowns

-

Free upgrades, like nicer finishes or appliances

Danielle Hale, Chief Economist at Realtor.com, explains why:

“New construction has been one of the steadiest parts of the housing market over the past few years, but builders are clearly responding to today’s affordability pressures and higher levels of existing-home inventory.”

Even builders, who many people think rarely negotiate, are competing on price and perks. They have been for over a year now. The same data shows this is the 15th straight month where more than 60% of builders have offered incentives to sweeten the deal. And that’s significant.

What This Means for Your Move

If you’re buying, this is a good time to ask. Whether you have your eye on an existing house or a newly built home, there’s a chance the seller or builder will meet you partway on price, terms, or both.

If you’re selling, expect buyers to ask. Even builders of brand-new homes are making concessions more often than not right now. Holding firm on every term could mean more time on the market, or a lost sale altogether.

Bottom Line

Sellers and builders are both giving buyers more to work with this year. A local agent can tell you what to expect in concessions and incentives based on inventory and competition in your local market.

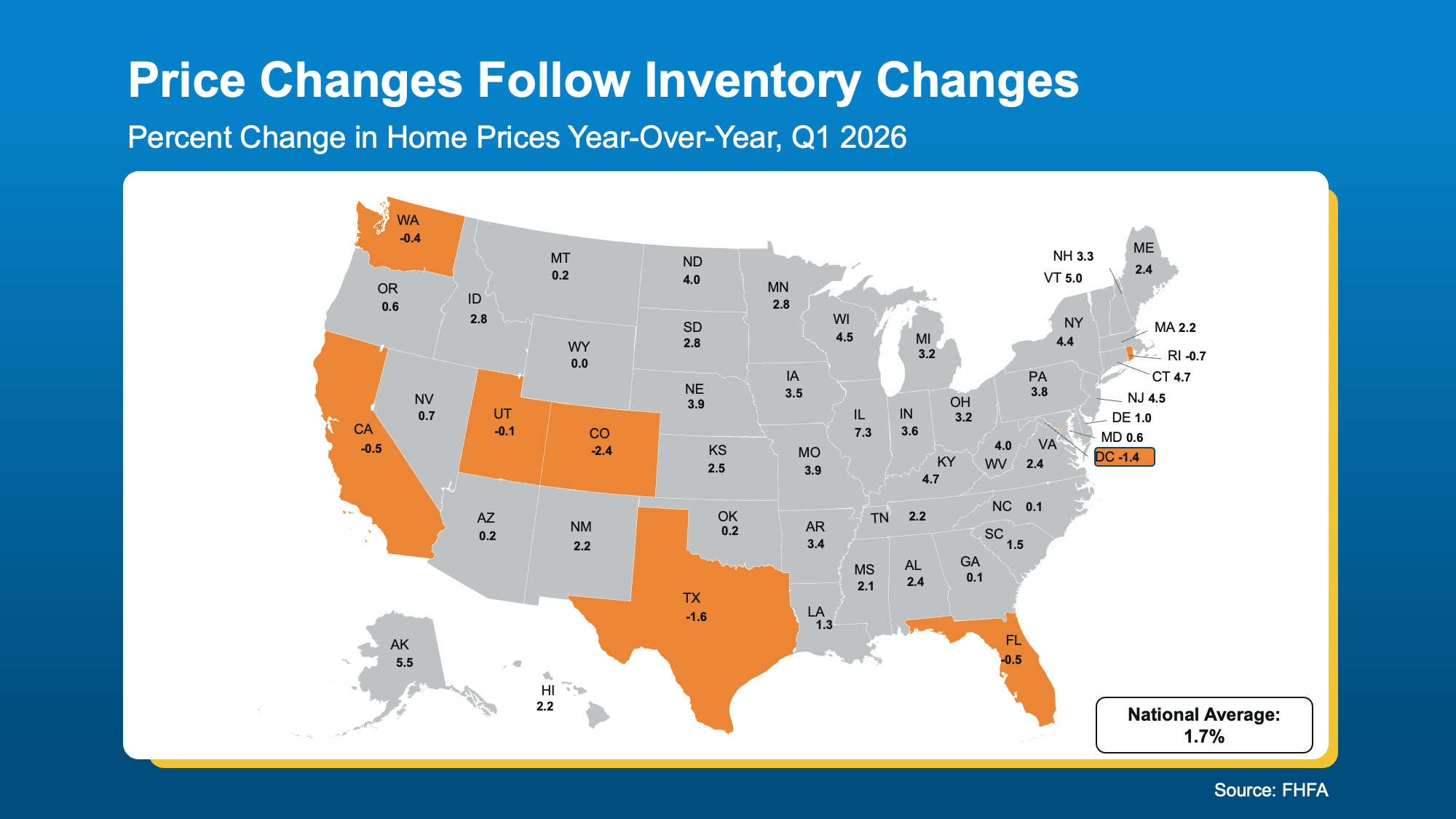

Now, let’s look at the latest Federal Housing Finance Agency (FHFA)

Now, let’s look at the latest Federal Housing Finance Agency (FHFA)