When you put your house on the market, you don’t just want it to sell. You want it to sell fast. But the thing is, nationally, it’s taking a little longer to sell lately. And that slowdown can feel frustrating if you want a fast process. Here’s what you need to realize.

In every market right now, there’s one clear exception:

Well-priced, well-presented homes are still selling, and it’s often faster than you’d expect.

If you can tap into that, you can still set yourself up to move quickly, too. Here’s how to get it done.

How Long It Takes To Sell Today

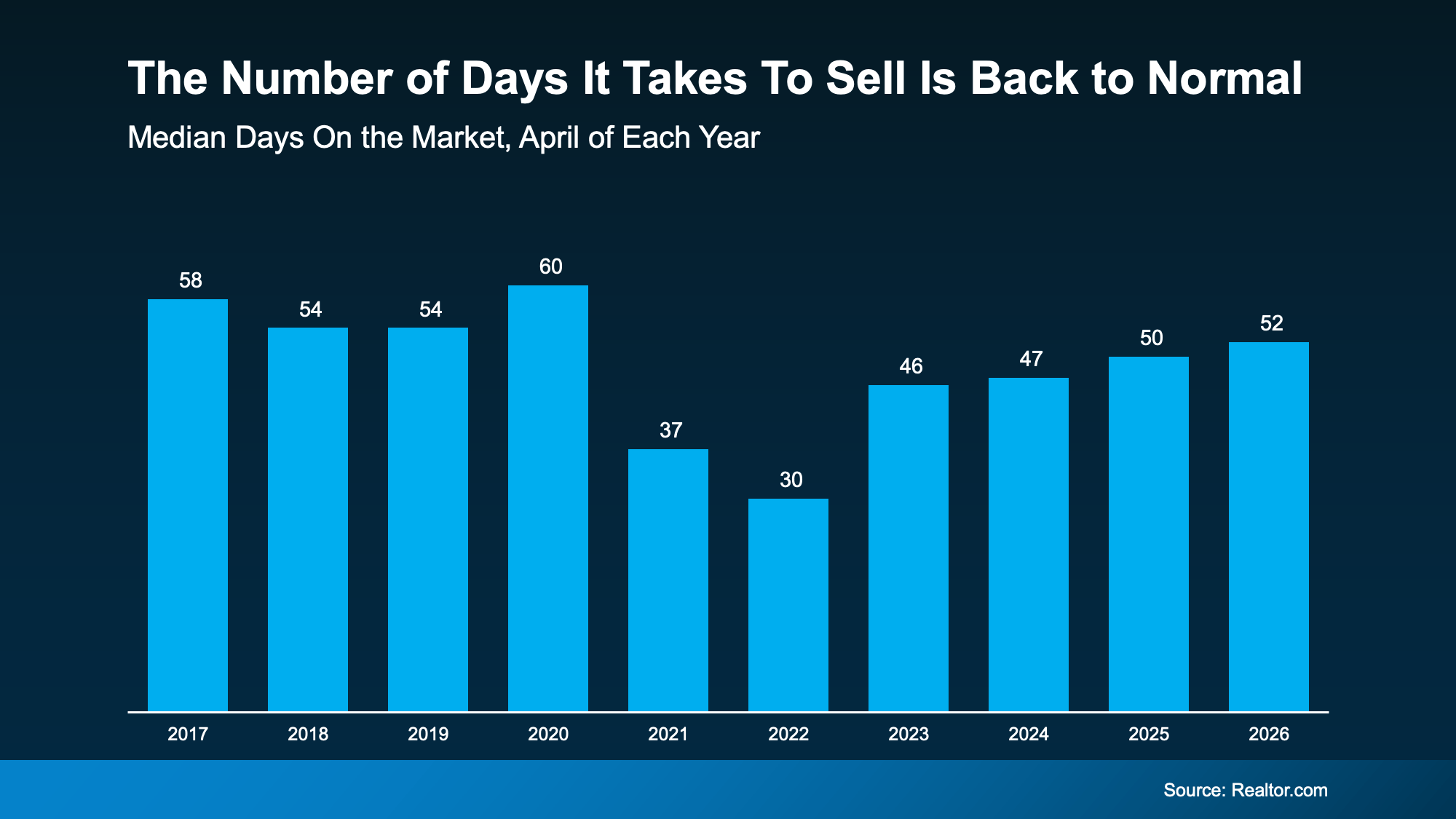

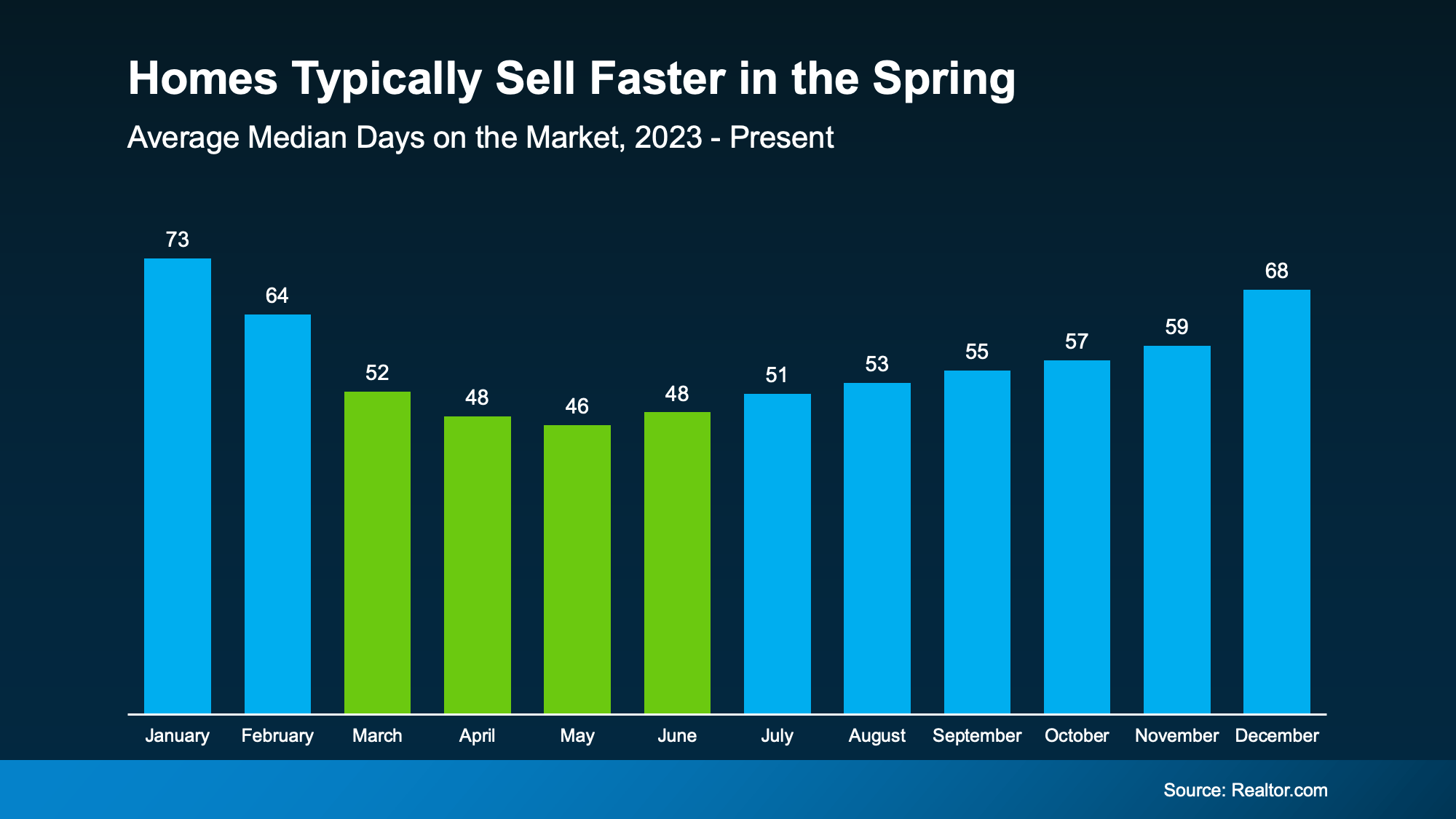

According to Realtor.com, homes are selling in about 52 days right now. That’s how long the process takes from the day it hits the market until closing day.

And while that may sound slow to you, it’s not slow. It’s normal.

That’s because it’s pretty much right in line with what it was during the last normal years in the market (see 2018-2019 in the graph below):

It just feels slow when you’re eager to move – or when you think back a few years to when homes seemed to sell almost instantly.

It just feels slow when you’re eager to move – or when you think back a few years to when homes seemed to sell almost instantly.

But here’s what matters most. The market is normalizing. Not at a standstill.

This is the norm for timing from start to finish. You may have an accepted offer in hand even faster than this.

Markets Where Homes Still Sell Quickly, Even Now

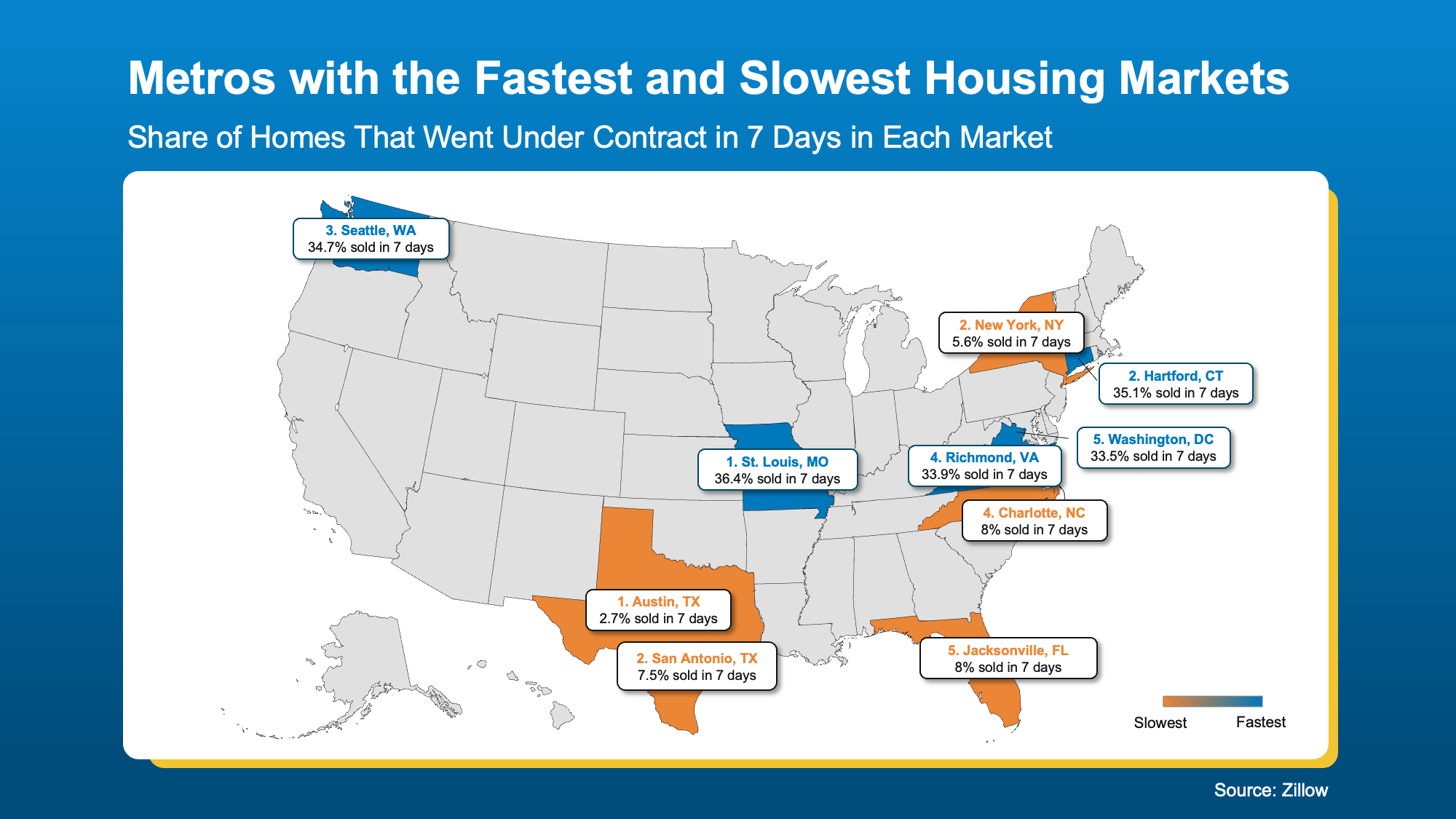

Zillow says the typical home will go “pending” or “under contract” in 19 days. Some homes even see it happen in as little as 7 days. It just depends on where you are – and how you prep your house.

So, don’t let the slowing pace of sales stress you out. Homes can still sell fast, if they’re positioned right.

Just to show you, here’s a quick look at some of the markets that are moving faster than the norm, according to Zillow (see map below). This’ll show you how different it can be based on where you live.

The key things you need to remember when looking at this visual:

The key things you need to remember when looking at this visual:

- It varies a lot based on where you live. Within the same state, individual neighborhoods or pockets may sell much faster than the norm.

- Even in slower moving states, you can still sell quickly. As the map shows, in those places there are still homes that go under contract in as little as a week.

So don’t worry about if your state made either list. As Orphe Divounguy, Senior Economist at Zillow, says:

“The cream of the crop is still selling fast, even in markets that have slowed considerably. . .”

The Big Reasons Some Homes Sit, and Some Sell Fast

And here’s the big secret. While location can definitely play a role, it’s not just about location. It’s about strategy.

Today’s buyers are paying attention to condition. They’re comparing photos, upgrades, layout, location, and price. And they’re choosing homes that feel move-in ready and well worth the value.

The homes that check those boxes? They’re not sitting for long – no matter where they are.

As the Wall Street Journal (WSJ) explains:

“. . . some homes are still flying off the shelves. These houses are often in the Midwest or Northeast, where the lack of new construction keeps a lid on supply. Certain homes in other markets are selling quickly, too, often when a home is move-in ready.”

Because in any market – hot or not – if a home is overpriced, needs too much work, or just doesn’t meet current buyer expectations, it’s not going to sell.

In this market, the sellers who win are the ones who get real about their house. They’re honest about how their home compares to other listings, realistic about price, and they work with an agent who truly understands today’s market and what it takes to sell.

When your agent knows how to price strategically, spotlight the strengths of your home, and move quickly when the market gives clear signals, that’s when the results follow.

Bottom Line

Today’s housing market rewards the right strategy. Because even in a slower area, the homes that are priced realistically and positioned well are still selling – sometimes faster than you may expect.

Connect with a local agent if you’re ready to make yours one of them.

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

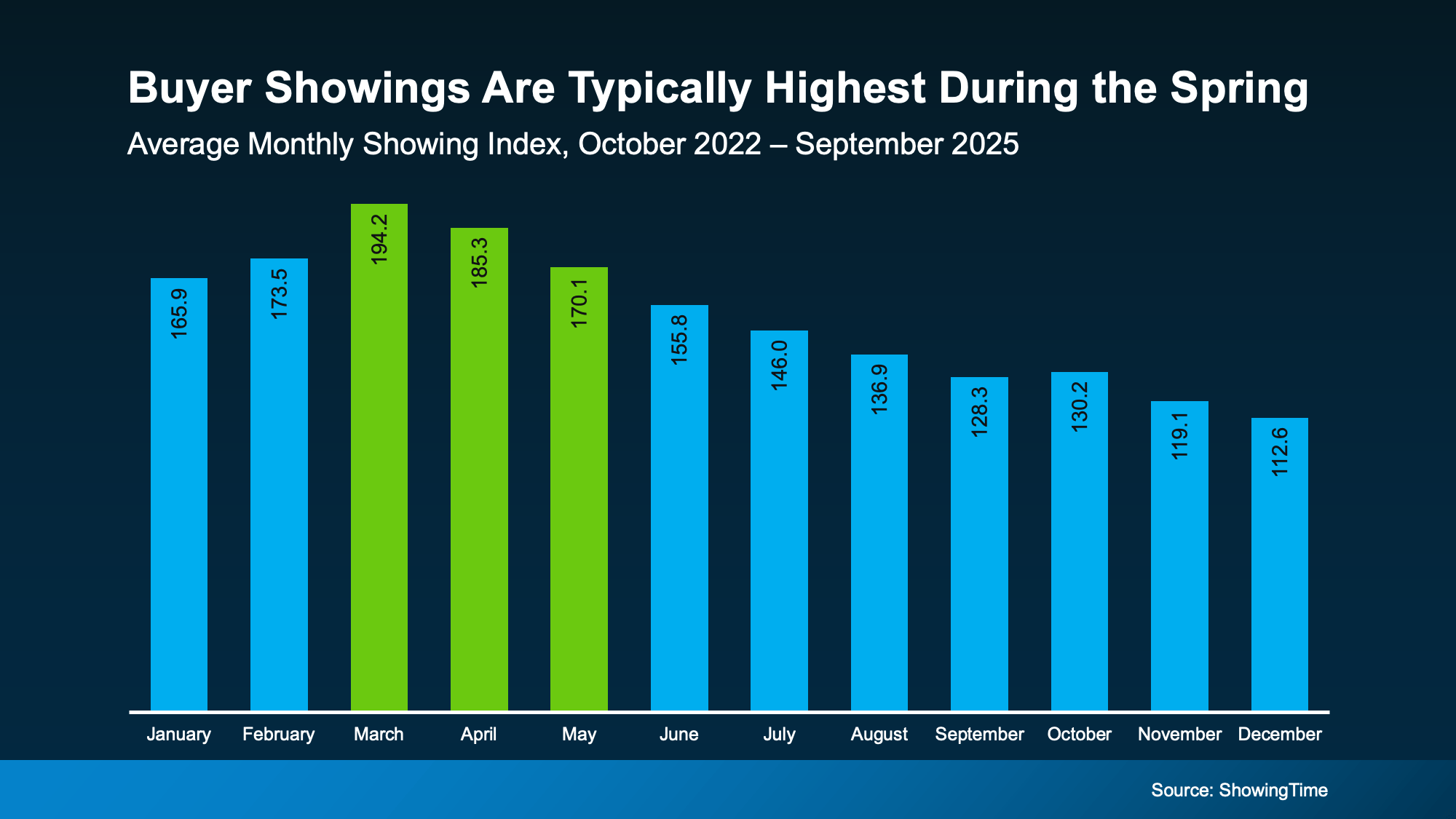

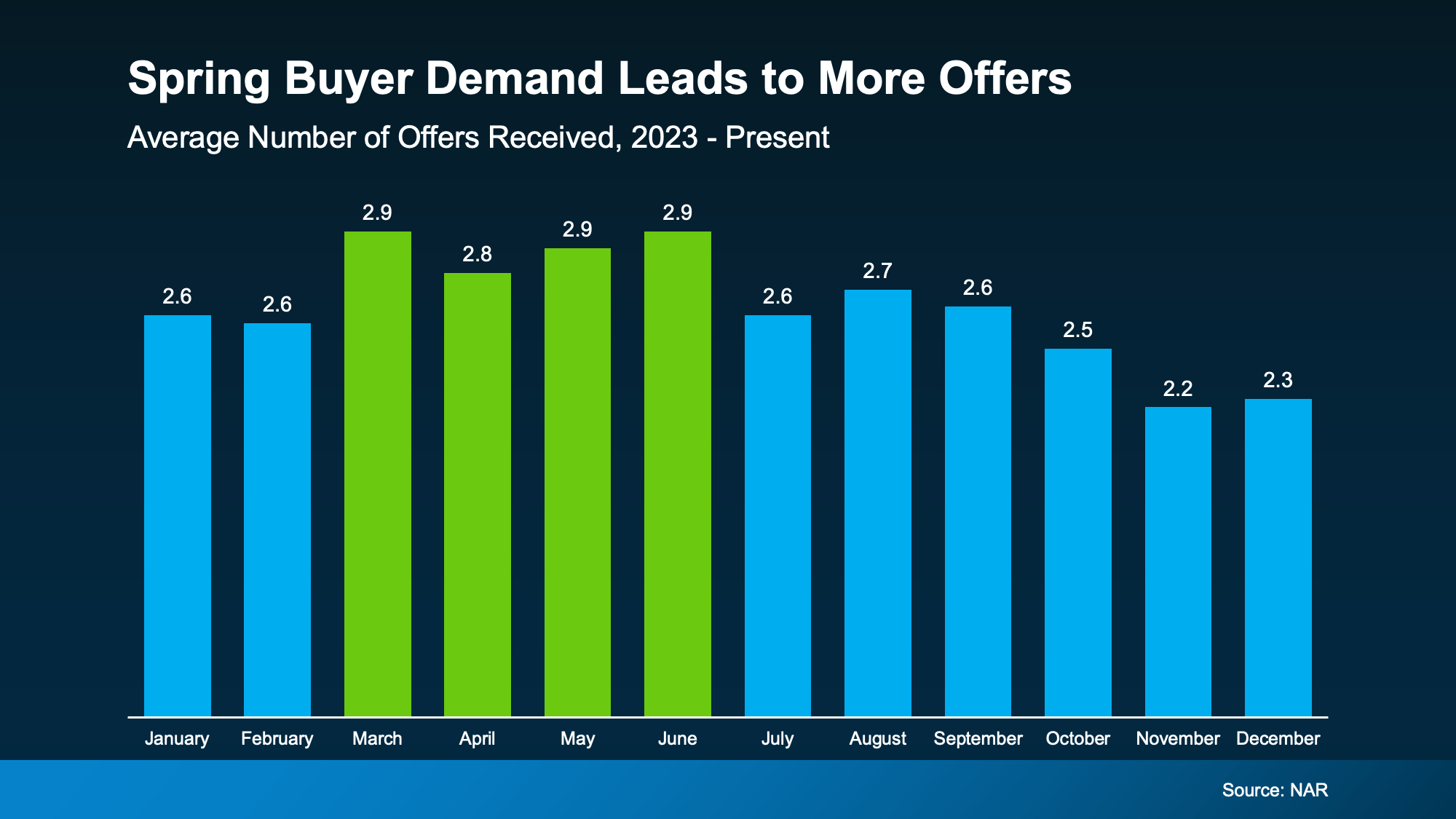

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that’s a difference you can feel.

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that’s a difference you can feel.