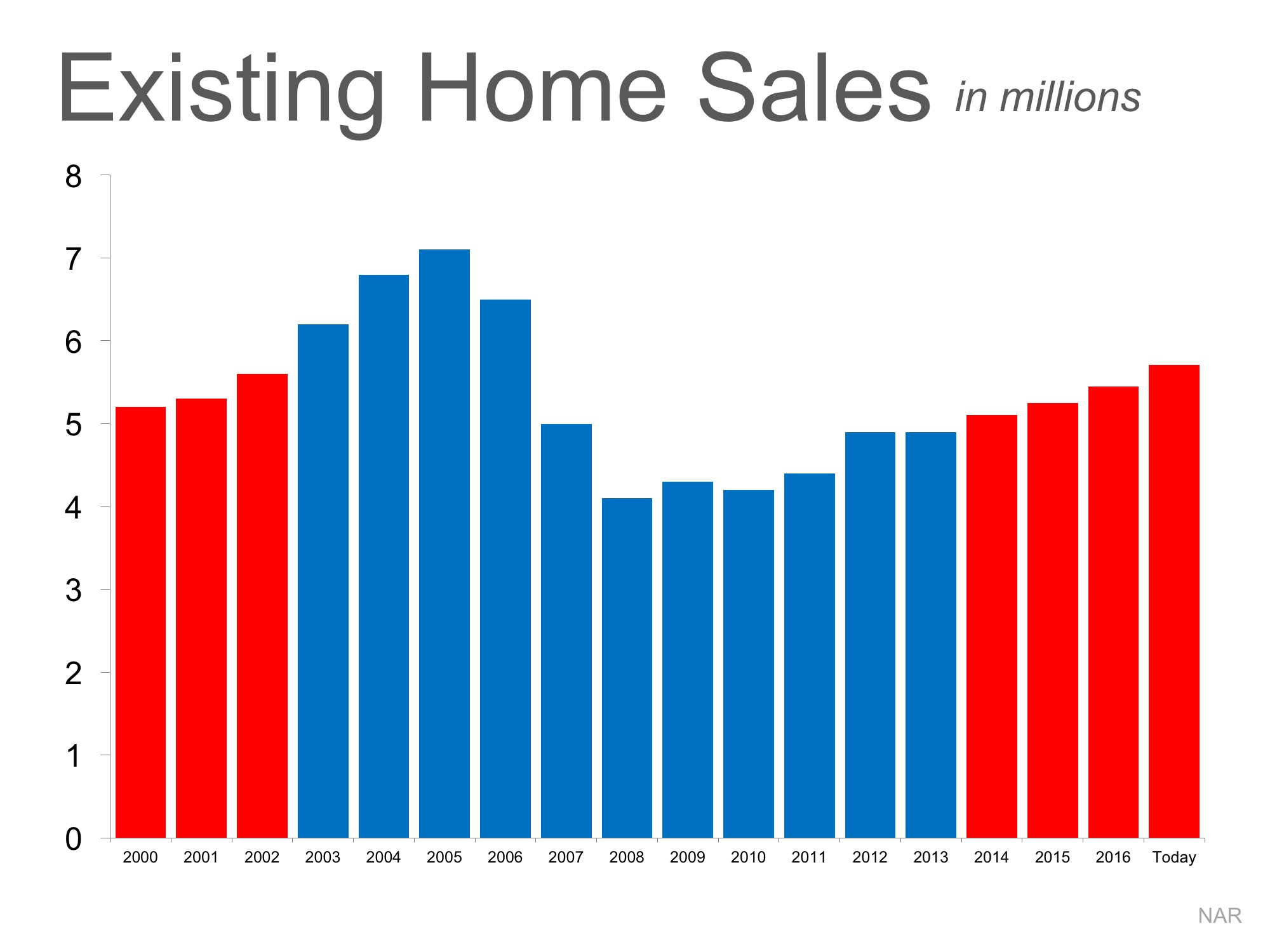

There are some experts questioning whether the current pace of residential home sales is maintainable. Are too many people buying homes like in 2004-2006? Are we headed for another housing crisis? Actually, if we look closely at the numbers, we can see that we are looking at a very healthy real estate market.

Why the concern?

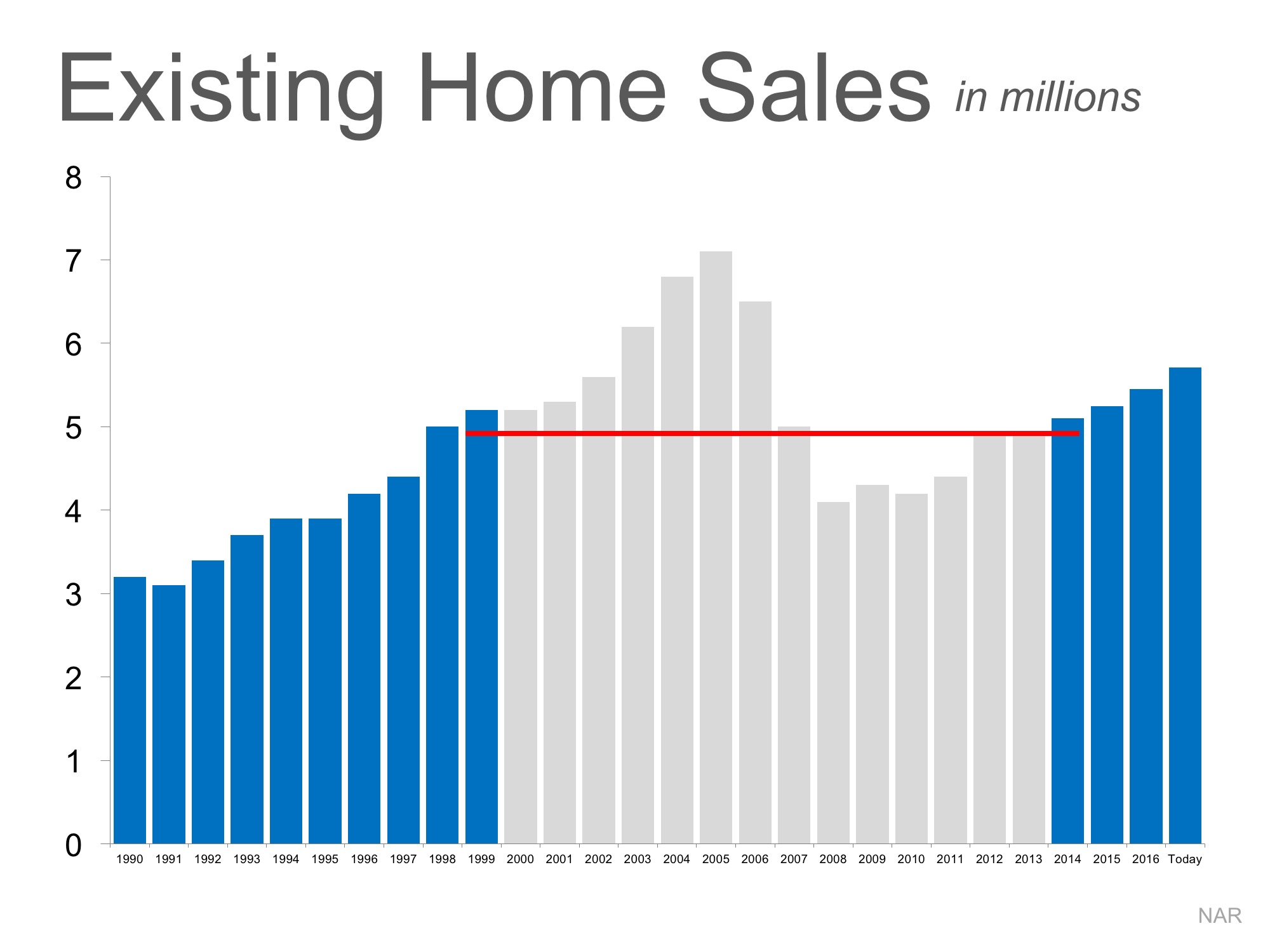

Some are looking at the last four years of home sales and comparing them to the three years just prior to the housing bubble. Looking at the graph below, we can understand that thinking.

However, if we go further back in history, we can see the real picture. After taking out the “boom & bust” years, the pace of sales is growing at quite a natural pace.

And new home sales are way below historic numbers. Dave Liniger, Re/Max CEO explains:

“We expect a seasonal uptick in sales this time of year and March certainly met and somewhat exceeded that expectation. We don’t anticipate the tightening inventory to ease up in most markets until new home construction can catch up to its pre-recession pace. Until then, sellers will enjoy a fast-paced market and buyers will need to work with their agents to get in the right home.”

Bottom Line

The current pace of residential home sales definitely seems maintainable.

![Slaying Home Buying Myths [INFOGRAPHIC] | Simplifying the Market](http://benningtonhomes.com/wp-content/uploads/2017/04/Slaying-Myths-STM-2.jpg)

![Is Your First Home Within Your Grasp? [INFOGRAPHIC] | Simplifying the Market](http://benningtonhomes.com/wp-content/uploads/2017/04/FTHB-Demographics-STM.jpg)