You may be hearing that a near-record number of homeowners are pulling their houses off the market. And if that headline has you thinking, “Wait… is something bad about to happen?” You’re not alone.

Because when people start stepping to the sidelines, it sounds like a warning sign that something’s coming – or that they realize something you don’t know.

Here’s the thing. This trend gets spun like it means the market is about to crash. But the data tells a more practical story.

What the Numbers Actually Say

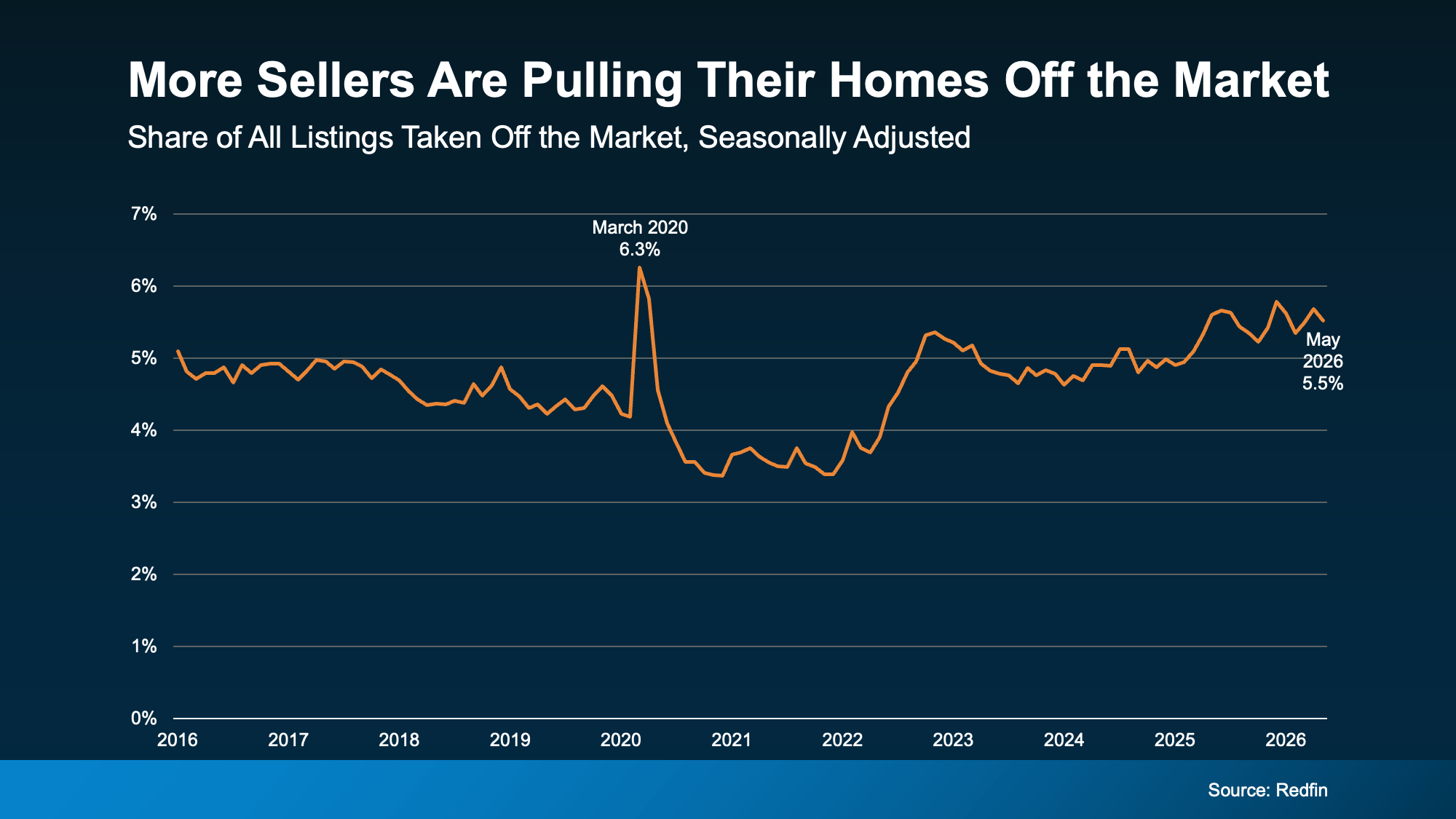

According to the latest data from Redfin, 5.5% of all listings were taken off the market in May. And it’s true that’s almost the highest it’s been since back in March 2020 (see graph below):

That can sound scary. But a lot of the fear comes from how this story gets told. “A near record number of sellers are pulling their listings” makes a great clickbait headline – and that sort of thing spreads fast, especially online. But sellers pull a house off the market for plenty of reasons that have nothing to do with a crash.

Redfin points to four main forces driving this trend:

-

Homes are taking longer to sell. When the pace slows down, some sellers get frustrated and decide to hold off.

-

The number of homes for sale is rising faster than demand. That means buyers have more options. And sellers who don’t price or prep right may not get many eyes on their house.

-

Some sellers still have pandemic-era price expectations. A price that would’ve worked a couple years ago may not match what today’s buyers will pay.

-

Economic uncertainty is making both buyers and sellers cautious. Buyers pause. Sellers second-guess. And that has an impact on overall sales volume and pace.

Notice what’s missing from that list? There isn’t a single mention of an impending market crash or price collapse.

This is about a shifting pace, more competition, and sellers deciding how they want to respond.

One Detail Most Headlines Leave Out

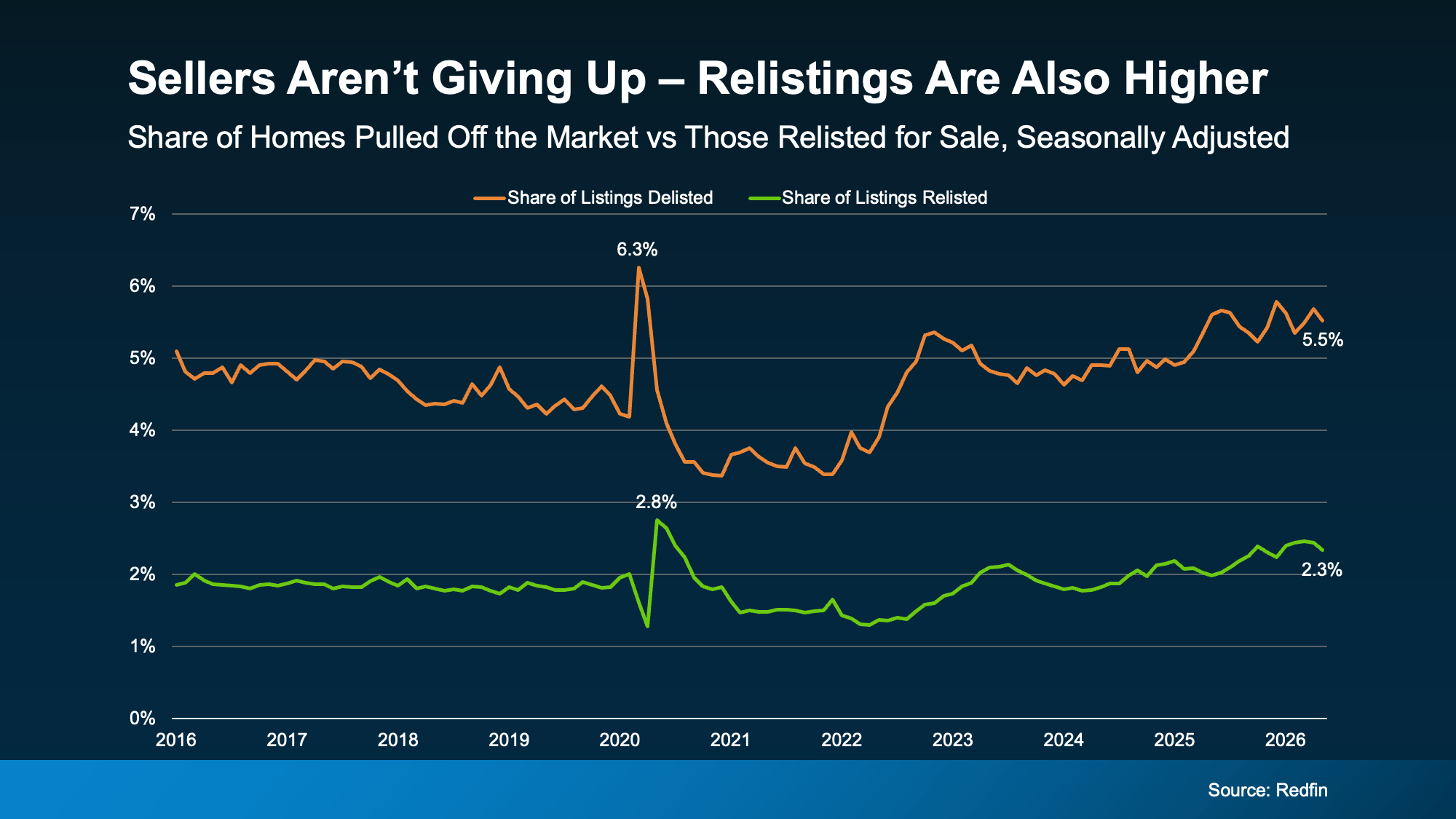

Want more peace of mind that this isn’t a crash? This next stat delivers. Yes, more sellers are taking their homes off the market. But Redfin also shows something you’re not going to see in social posts…

The number of re-listings is growing too.

While more sellers are pulling their listings, more are also deciding to give selling a second shot too. This is pretty much the highest re-listings have been since the pandemic hit.

While 5.5% got pulled in May, 2.3% were also put back on the market (see graph below):

That’s a signal sellers aren’t giving up or running away in large numbers.

Some are simply stepping away briefly before deciding to try again. That tells you this often isn’t a permanent decision. In many cases, it’s a pause – and the seller comes back with a different approach.

A lot of the time that change in the overall strategy is all that’s needed to finally get a house sold.

And just in case you need more proof this isn’t a reason to worry, check this out. Buyer activity may be starting to pick back up – and that could bring more sellers back in or, at least, prevent some sellers from pulling back.

The National Association of Realtors (NAR) reports existing home sales increased 3.2% in May. That’s the biggest increase since December. As the Wall Street Journal puts it:

“Home sales in May posted the biggest rise this year, a sign that the housing market’s crucial spring selling season may be showing signs of life after a sluggish start.”

That doesn’t sound like a market in trouble.

Bottom Line

If you’re seeing headlines about how a record number of sellers are taking their homes off the market, don’t panic. It’s not a warning of an impending crash. It’s a market adjusting.

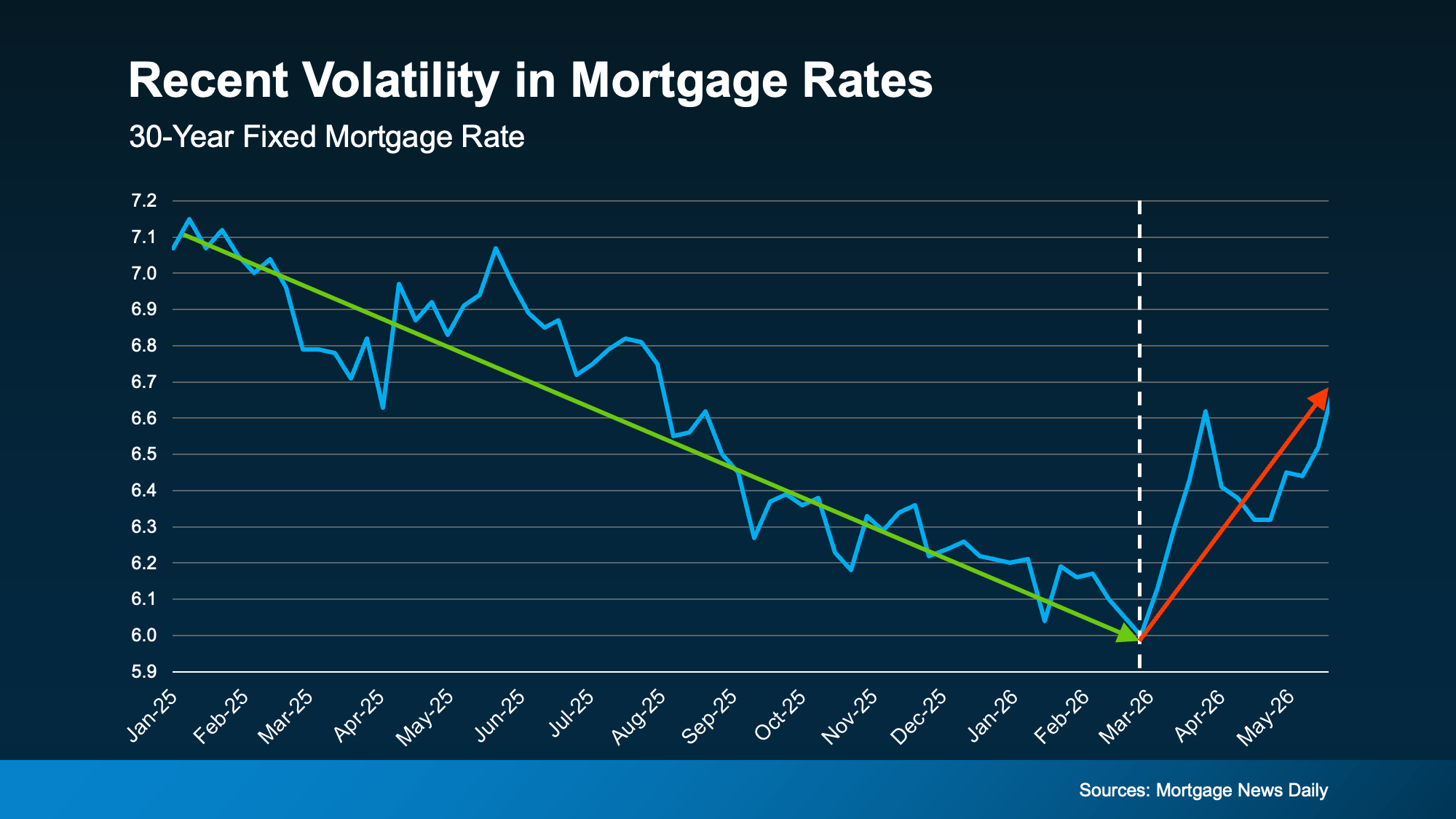

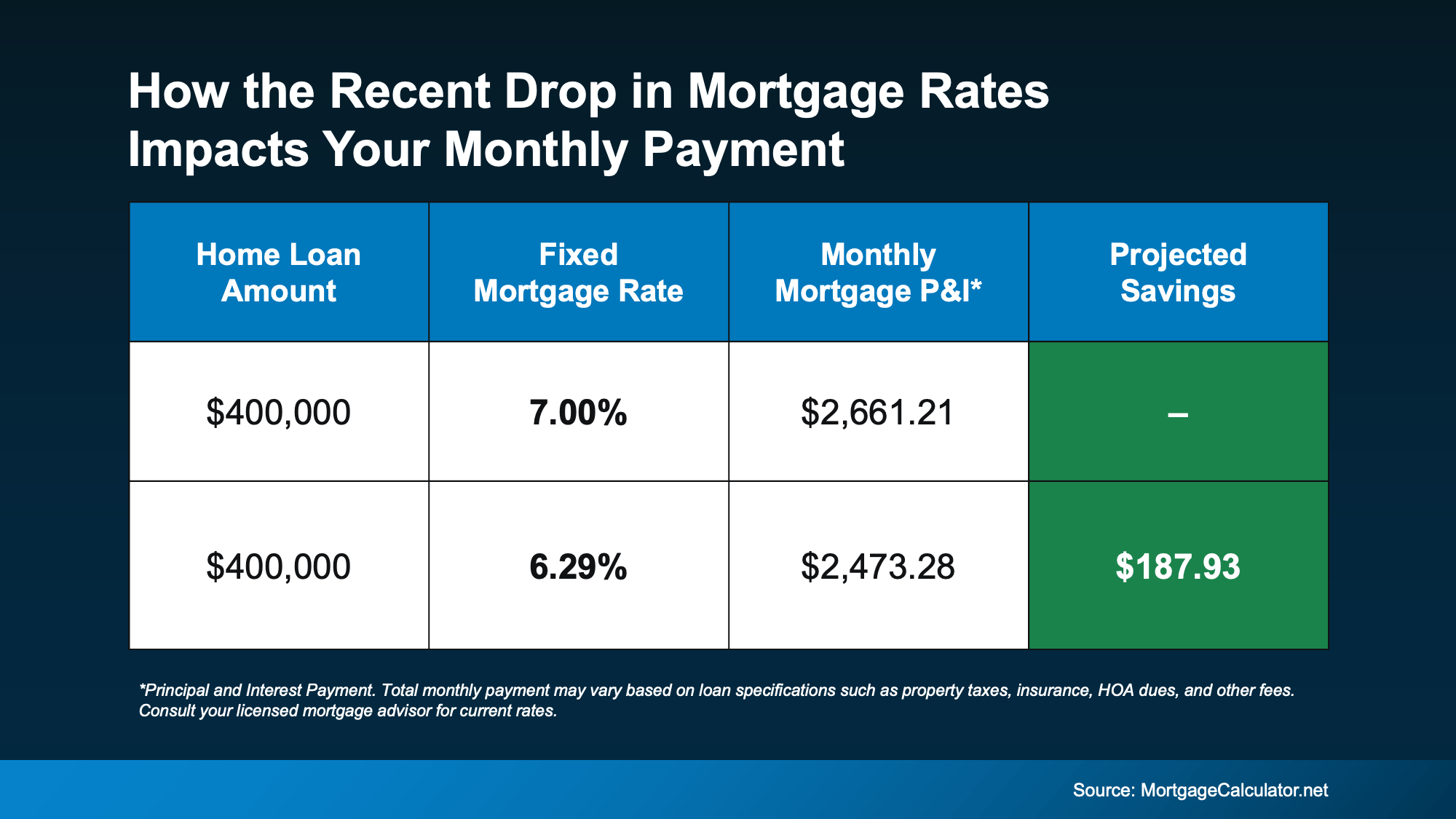

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it’s probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.