If buying a home is on your radar, you’ve probably been keeping an eye on mortgage rates and home prices. But don’t forget about homeowners insurance.

Homeowners insurance has always been part of owning a home. But over the past few years, it’s become a larger expense for many homeowners – something that’s especially frustrating when affordability already feels tight.

The good news? While premiums are still rising, the latest data shows those increases are beginning to slow. Here’s what buyers should know.

Home Insurance Costs Have Gone Up

You’ve probably heard stories from friends or family about their premiums going up. And that’s not really a surprise when you consider data from the Pew Research Center shows 71% of homeowners say their insurance costs have gone up over the past few years.

While no one likes rising costs, knowing what to expect can help you plan ahead. Your first insurance payment is typically included in your closing costs, but after that it’ll become part of your monthly housing expenses.

Getting an insurance quote early can help you build a more realistic budget and avoid surprises later.

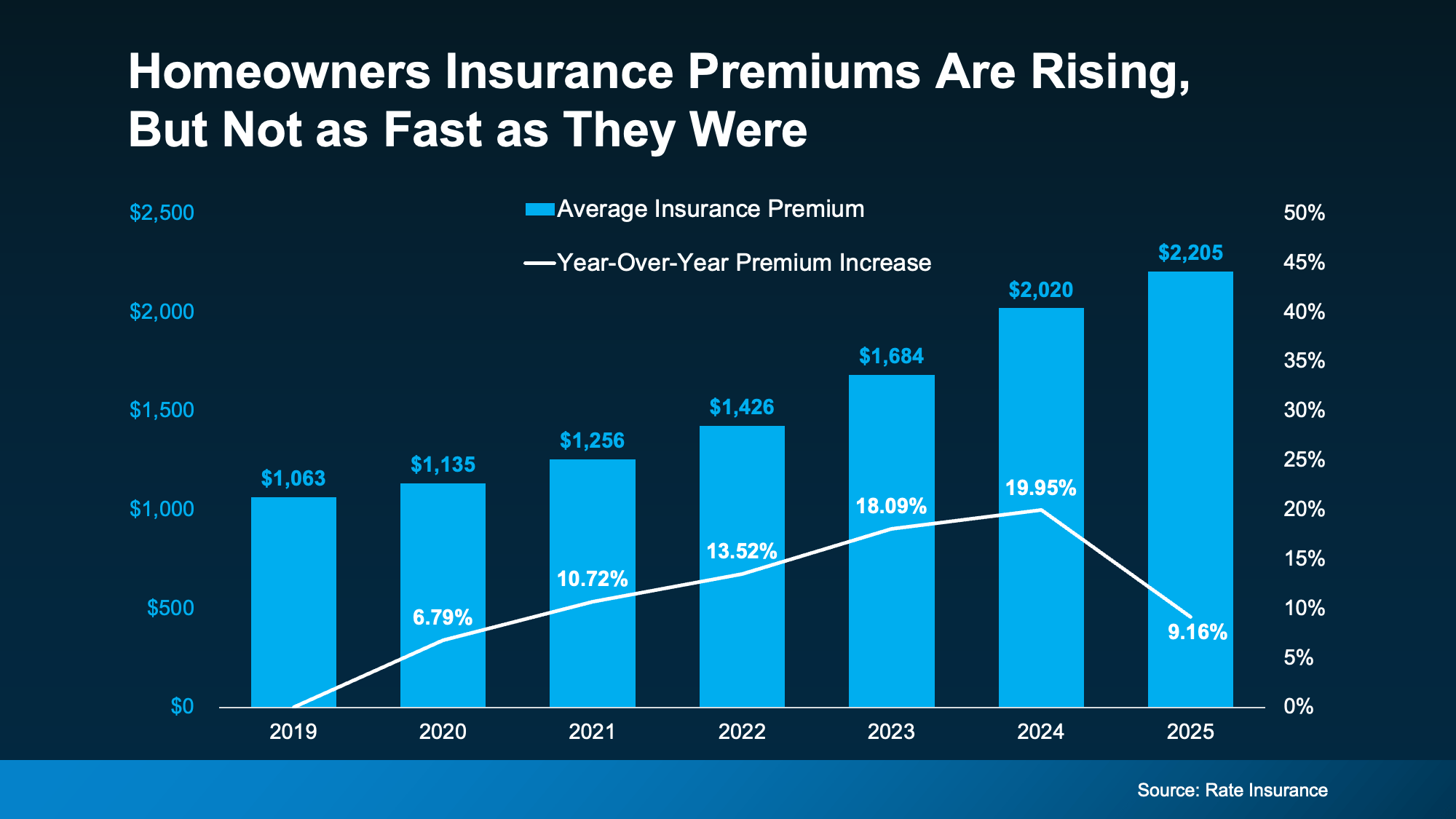

Premiums Are Rising, But Not as Fast as They Were

Most of the headlines focus on how home insurance is getting more expensive. And that’s true. But here’s the part that’s easy to miss.

Insurance premiums are still rising.

But they’re not rising as fast as they were.

According to the latest report from Rate Insurance, 2025 saw the first slowdown in annual premium increases since 2019 (see graph below):

That doesn’t mean premiums are getting cheaper. It simply means the rapid increases of the past several years may finally be starting to ease – a small but welcome step in the right direction.

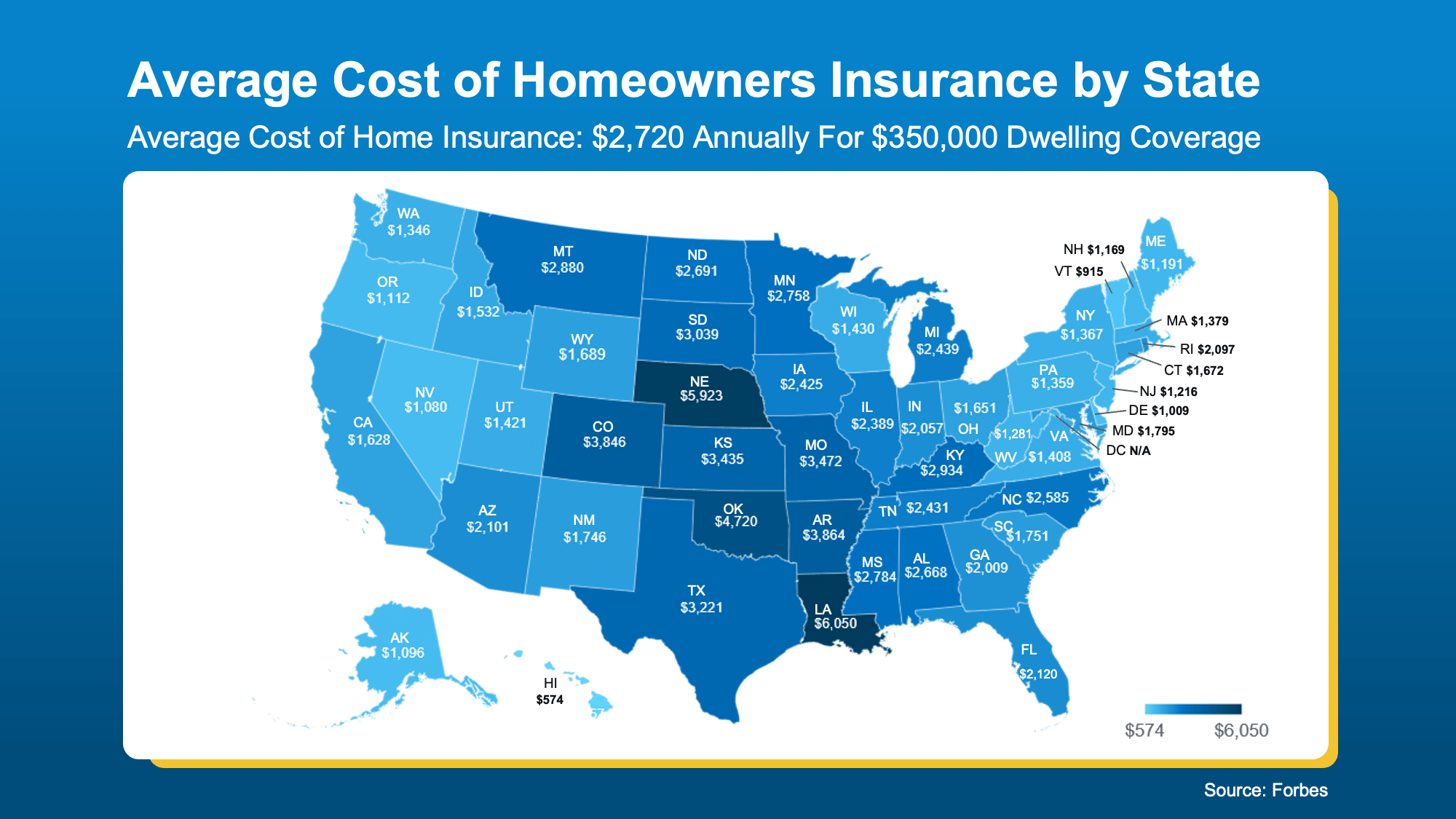

But what you’ll pay in one part of the country can look very different from what someone pays somewhere else.

Where You Buy Can Make a Big Difference

Insurance costs vary because some parts of the country experience more claims than others. That’s why it’s important to look at what’s happening locally.

Your premium will depend on things like where you’re buying, the home itself, and the coverage you choose.

Forbes data can give a rough idea of your state’s typical premiums. Check out the map below – the darker the blue, the higher the costs tend to be in that state:

Ways To Lower Your Costs

While you can’t control every cost that comes with buying a home, you can control how prepared you are. If you’re crunching the numbers and trying to find ways to save, Insurify and NerdWallet offer these tips that can help you get the best insurance price possible:

-

Shop Around – Compare quotes from multiple companies.

-

Bundle Policies – Combine home and auto to see if a bundle price is cheaper.

-

Ask If There Are Discounts – Don’t miss out on savings you may qualify for.

-

Highlight Upgrades – Features like a new roof or storm windows can cut costs.

-

Improve Your Credit – A stronger credit score can mean better premiums.

One of the smartest things you can do is get an insurance quote before you make an offer. That way, you’ll know what your monthly housing costs are likely to be before you commit.

An insurance professional can walk you through your options and help you find coverage that fits both your needs and your budget.

Bottom Line

Homeowners insurance has become a bigger part of the homebuying conversation. But it doesn’t have to become a bigger source of stress.

The key is knowing what to expect before you buy. Get an insurance quote early, factor it into your budget, and lean on trusted local professionals to help you make the most informed decision possible.

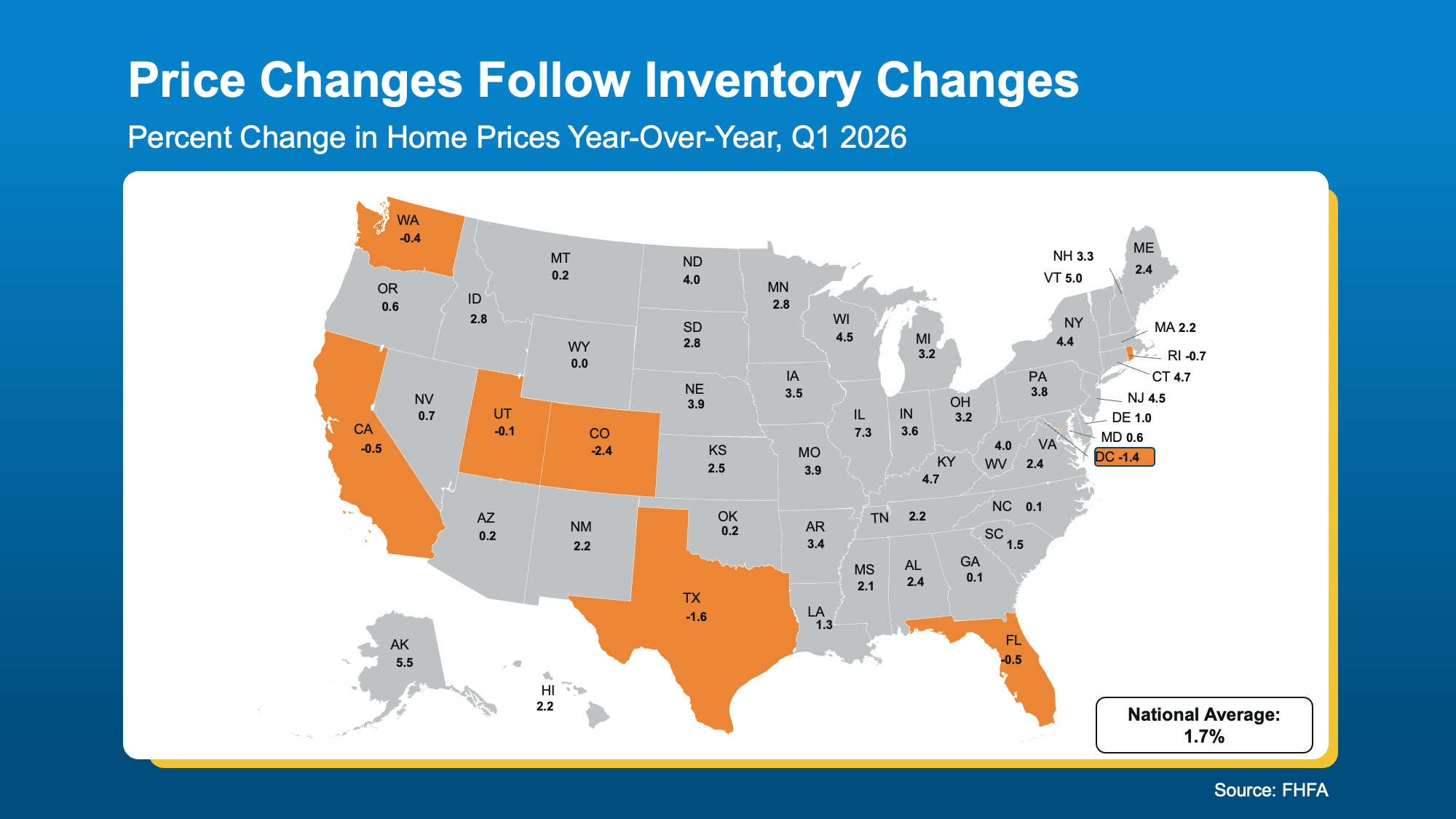

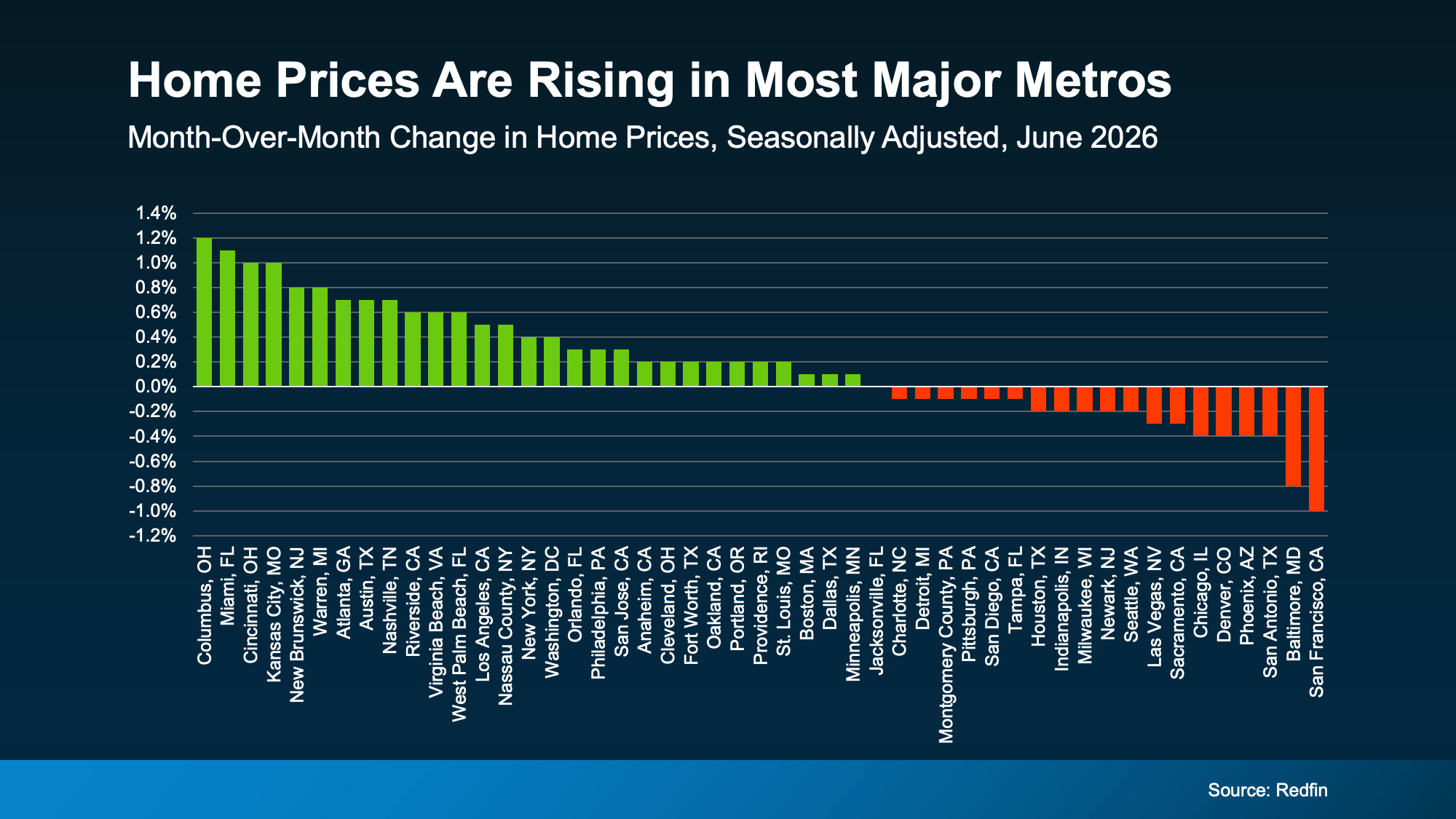

Now, let’s look at the latest Federal Housing Finance Agency (FHFA)

Now, let’s look at the latest Federal Housing Finance Agency (FHFA)