If you’re trying to sell your house, you may be looking at this spring season as the sweet spot – and you’re not wrong. We’re still in a seller’s market because there are so few homes for sale right now. And historically, this is the time of year when more buyers move, and competition ticks up. That makes this an exciting time to put up that for sale sign.

But while conditions are great for sellers like you, you’ll still want to be strategic when it comes time to set your asking price. That’s because pricing your house too high may actually cost you in the long run.

The Downside of Overpricing Your House

The asking price for your house sends a message to potential buyers. From the moment they see your listing, the price and the photos are what’s going to make the biggest first impression. And, if it’s priced too high, you may turn people away. As an article from U.S. News Real Estate says:

“Even in a hot market where there are more buyers than houses available for sale, buyers aren’t going to pay attention to a home with an inflated asking price.”

That’s because no homebuyer wants to pay more than they have to, especially not today. Many are already feeling the pinch on their budget due to ongoing home price appreciation and today’s mortgage rates. And if they think your house is overpriced, they may write it off without even stepping foot in the front door, or simply won’t make an offer if they think it’s priced too high.

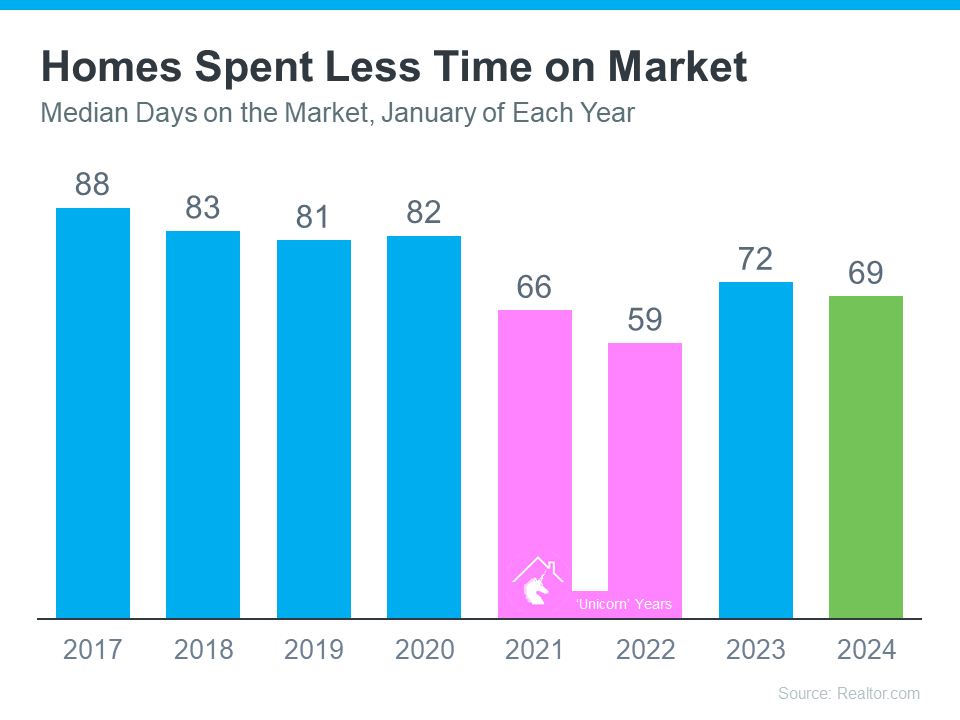

If that happens, it’s going to take longer to sell. And ideally you don’t want to have to think about doing a price drop to try to re-ignite interest in your house. Why? Some buyers will see the price cut as a red flag and wonder why the price was reduced, or they’ll think something is wrong with the house the longer it sits. As an article from Forbes explains:

“It’s not only the price of an overpriced home that turns buyers off. There’s also another negative component that kicks in. . . . if your listing just sits there and accumulates days on the market, it will not be a good look. . . . buyers won’t necessarily ask anyone what’s wrong with the home. They’ll just assume that something is indeed wrong, and will skip over the property and view more recent listings.”

Your Agent’s Role in Setting the Right Price

Instead, pricing it at or just below current market value from the start is a much better strategy. So how do you find that ideal asking price? You lean on the pros. Only an agent has the expertise needed to research and figure out the current market value for your home.

They’ll factor in the condition of your house, any upgrades you’ve made, and what other houses like yours are selling for in your area. And they’ll use all of that information to find that target number. The right price will bring in more buyers and make it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly.

Bottom Line

Even though you want to bring in top dollar when you sell, setting the asking price too high may deter buyers and slow down the sales process.

Connect with a local real estate agent to find the right price for your house, so we can maximize your profit and still draw in eager buyers willing to make competitive offers.