Be honest. Have you started looking at homes online yet? If you have, it’s already time to get pre-approved. Because here’s what not enough people know.

If buying a home is on your radar – even if it’s more of a someday plan than a right now plan – you don’t want to wait until later on in the process to tackle this step.

No matter what you’ve heard, pre-approval isn’t about commitment. It’s about clarity.

And here are the two big ways pre-approval sets you up for success.

You Know Your Numbers Up Front

During the pre-approval process, a lender will walk through your finances and tell you what you can borrow based on your income, debts, credit score, and more. And once you have that number, your search becomes a lot more focused.

With a mortgage pre-approval, you know what you can borrow, so it’s easier to figure out your ideal price point, and what you can actually afford. And that clarity is key.

Because if you just start browsing online and just guess at your price point, you run the risk of falling for a house that’s outside of your price range – or missing out on ones that aren’t.

You want this number to be clearly defined before your search. Here’s why.

You Can Move Quickly When You Find the One

This is how a lot of home searches go today. You scroll through listings just to see what’s out there, and then it happens. You fall in love with something you’ve seen online.

If you’re already pre-approved? You’re probably in great shape.

But if you’re not…

Instead of being able to jump on that house and quickly make an offer, you have to scramble to get a lender, gather the financial documents, and then submit the necessary pre-approval paperwork first. And while you’re waiting to hear back from your lender, someone else who’s more prepared could beat you to the house. As Bankrate explains:

“The best time to get a mortgage preapproval is before you start looking for a home. If you find a home you love but don’t have a preapproval in hand, you likely won’t have time to get preapproved before you need to make an offer . . .”

And that’s avoidable, with the right prep.

Because while you can’t control when the right home shows up, you can be ready for it. Think of it like showing up to the starting line with your shoes tied and your warm-up done – while everyone else is still looking for parking.

It’s not about rushing your timeline. It’s about removing the delay between finding the right home and being able to move on it.

One Thing You Need To Know About Pre-Approvals

Speaking of timing, pre-approvals do have an expiration date. So, be sure to ask your lender how long it’s good for. The Mortgage Reports explains:

“Mortgage preapproval letters are typically valid for anywhere from 30 to 90 days. However, a preapproval can be updated and extended if the lender re-checks your information.”

Doing the right prep and knowing this information can make the whole process a lot smoother.

You don’t have to be ready to buy to be ready to buy.

Getting pre-approved doesn’t mean you’re committing to buy right now. It just means you’ve taken a step to understand your numbers. And when a home catches your attention, you’re prepped and good to go.

Bottom Line

Ask yourself this: if your perfect home popped up tomorrow, would you be ready to make a move?

If the answer is no and you want to buy, it may be time to get pre-approved. You don’t feel behind before your search even officially kicks off.

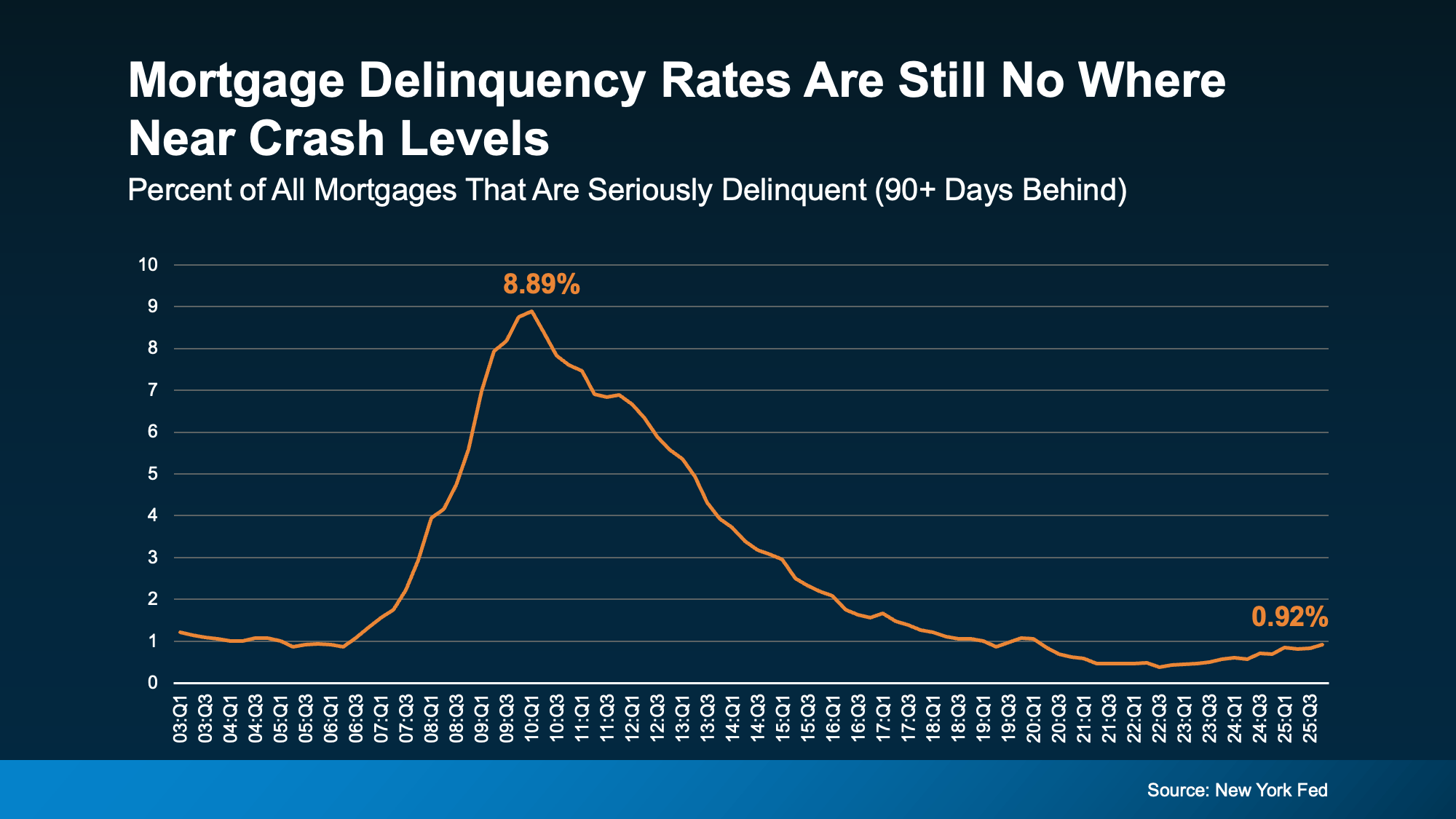

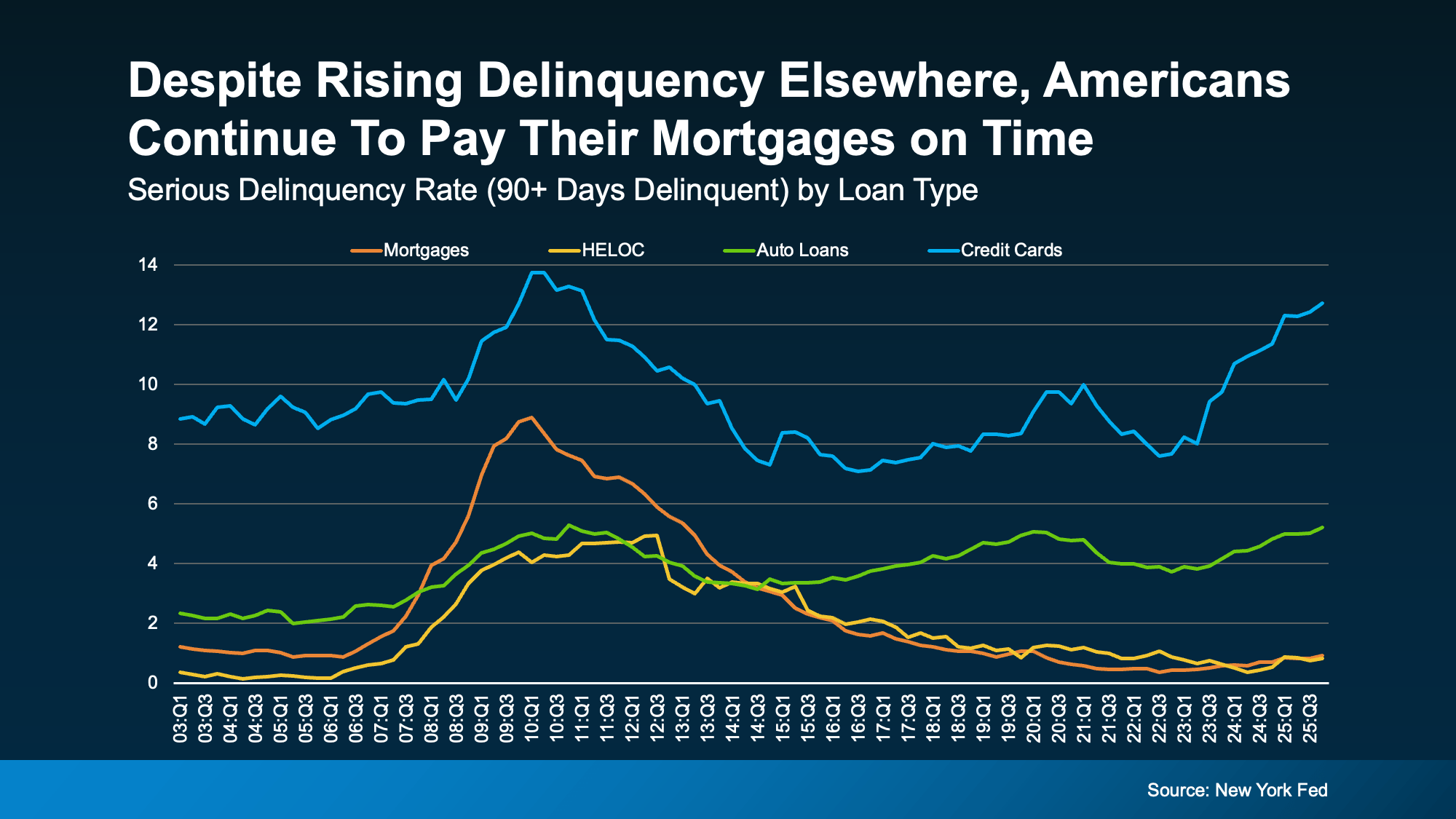

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.