Whether you’ve owned a home before, or you’re ready to jump into homeownership for the first time, there are always a lot of questions swirling around about what is truly required for a down payment, and how to best source down payment assistance. Let’s tackle these two today.

1. How much do you really need for a down payment?

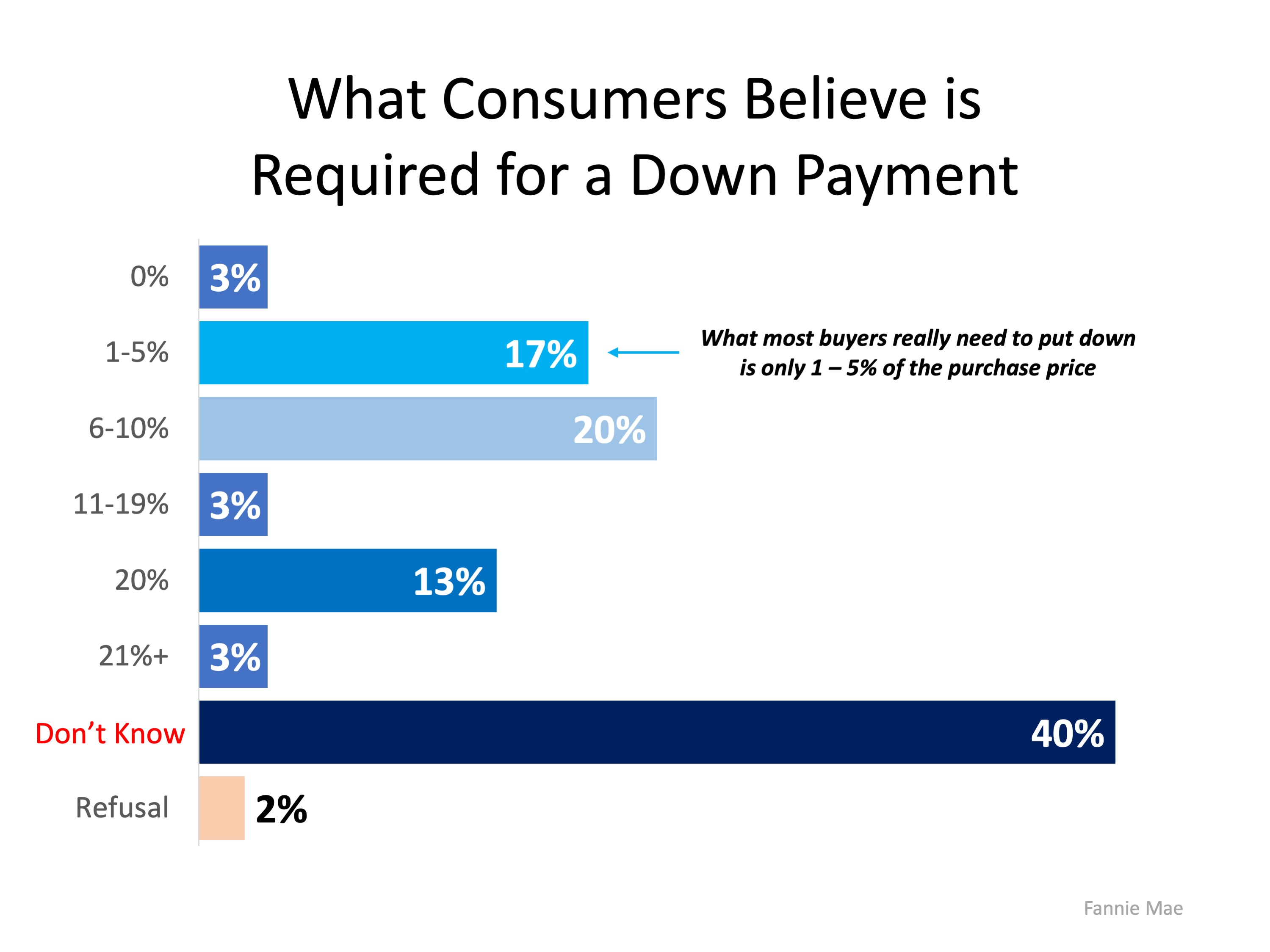

There is a long-standing misconception about down payment requirements. A survey from Fannie Mae shows only 17% of consumers know the minimum options are actually between 1 – 5% of the purchase price and 40% don’t know how much they need at all. There are many mortgage loans available that require as little as 3% down for first-time buyers, and some ask for only 3.5% down from repeat buyers. There are even loans available for Veterans that provide 0% down payment options too.

There are many mortgage loans available that require as little as 3% down for first-time buyers, and some ask for only 3.5% down from repeat buyers. There are even loans available for Veterans that provide 0% down payment options too.

We’ve mentioned recently that you don’t need to come up with a 20% down payment to buy, and we’ve also shared how quickly you can save for a 3% or 10% down payment, depending on where you live. If you’re planning to put down just 3%, the research shows it may be possible in most states to have enough saved for a down payment in less than a year. That puts homeownership in a much closer reach for many potential buyers, maybe even you!

2. How can I get help with my down payment?

Regardless of the loans available, many buyers still need assistance with a down payment. The great news is, there are a lot of ways to tap into down payment assistance options. Here are just a couple of them:

Assistance from Family Members

The National Association of Realtors (NAR) said, “a third of recent first-time buyers received down payment assistance from family members.” They also mentioned, “the average net worth of those aged 75 and over stands at $264,800…They just might offer the boost the next generation needs to become homeowners.”

That means one of the ways to find help with a down payment is to accept a gift from a family member. If this is an option for you, make sure you talk to your loan officer before you accept the money, to ensure you document the process the way it is required by your loan. This way, it will be received properly and you can still potentially qualify.

Down Payment Assistance Programs

The reality is, not everyone has a loved one or a family member who can provide help with a down payment. There are, however, more than 2,500 down payment assistance programs available (by local areas like city, county, or neighborhood), and some of them are even specifically for first-time buyers.

The gap, as mentioned in the same survey, is “only 23% of consumers are familiar with low down payment programs.”

That’s why it is so important to get familiar with these options by doing your homework before you plan to buy a home. Determine what is available in the area where you ultimately want to live, so you have all the details you need to take advantage of the down payment assistance option that is best for your family.

Bottom Line

If buying a home is one of your long-term goals, you may be able to get there sooner than you think by tapping into one of the many down payment assistance programs available.

![Rent Vs. Own [INFOGRAPHIC] | Simplifying The Market](http://benningtonhomes.com/wp-content/uploads/2019/08/20190809-Share-KCM-549x300.jpg)

![Rent Vs. Own [INFOGRAPHIC] | Simplifying The Market](http://benningtonhomes.com/wp-content/uploads/2019/08/20190809-MEM.jpg)

![Is Your First Home Now Within Your Grasp? [INFOGRAPHIC] | Simplifying the Market](http://benningtonhomes.com/wp-content/uploads/2019/07/20190621-Share-STM-549x300-1.jpg)

![Is Your First Home Now Within Your Grasp? [INFOGRAPHIC] | Simplifying the Market](http://benningtonhomes.com/wp-content/uploads/2019/07/FTHB-Demographics-ENG-MEM-1.jpg)